By Matt Walker

What a difference a year makes. Vendor revenues in the telco network infrastructure market (telco NI) grew again in 2Q21, rising 5.1% YoY after a 10.0% jump in 1Q21. Overall for the first half of 2021, telco NI vendor revenues amounted to $110.4 billion (B), up 7.4% from the 1H20 period. Some of the growth is compensating for a weak 1H20 hit by COVID’s initial spread, and some of the growth is due to depreciation of the US dollar. But there is also an uptick in telco spending across multiple segments and geographies. Telco capex for the first half of 2021 rose to $151.1B, up 9.8% YoY.

Telcos are beginning to scale up their 5G networks and fiber access spending is strong; transport network spending is also looking up in markets where 5G penetration is high and traffic growth requires capacity increases further upstream. Vendors who help telcos migrate to cloud-based architectures and services are seeing strong demand. Deployment of stand-alone 5G core networks is just beginning, but as this spreads a number of vendors benefit, including those in the core/edge router market. Automation continues to be a key theme for telco investment as well, helping vendors with strong offerings in this area, especially those able to help telcos revamp processes to leverage new technologies.

Changes in coverage in 1H21

In the 1Q21 edition of MTN Consulting’s “Telecom’s Biggest Vendors” series, we added four suppliers: Airspan, Alphabet (GCP), Amazon (AWS), and Microsoft (Azure). Airspan is an important supplier in the open RAN market, and claims customer relationships in over 100 countries. AWS, Azure, and GCP are cloud services providers who have taken on an increasingly important role in the telecom sector, supporting telcos with core network functions, providing digital transformation services, and collaborating on service development and delivery. No further changes to coverage were made in 2Q21.

Telco capex grew 15% YoY in 2Q21, opex up 14%

Telco NI vendor revenues are fed by a mix of telco capex and opex budgets. In 2Q21, global telecom operator capex grew at the surprisingly strong rate of 15% YoY, after a 5% climb in 1Q21. Opex (excluding depreciation & amortization) increased by 7% in 1Q21 and 14% in 2Q21. This growth is consistent with directions in the telco NI vendor market.

Within the overall telco opex budget, telcos are having success in cutting their sales & marketing and G&A spending, as telcos adjust to working from home and accelerate the migration of sales & support to digital platforms. Labor costs are a big part of telco opex (and rising), and automation is a key area of investment in 2021 for nearly all major telcos. Numerous telcos are reporting that network operations is taking up a larger portion of the opex pie. This is important because vendors are increasingly selling into opex budgets within their telco customers, not just capex budgets. That’s especially true on the services and software sides. Webscale operators’ sales of software licenses to telcos are growing, and starting to bump up competitively against the more traditional telco-centric vendors like Amdocs and CSG.

Leaderboard largely unchanged but Huawei is slipping

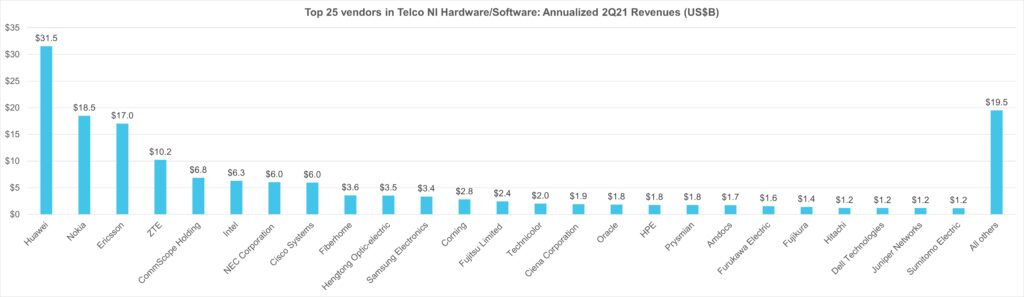

The market share leaders in the global telco NI market remain Huawei, Ericsson, Nokia, and ZTE, who are also the top providers of 5G infrastructure. After these top 4, China Comservice took the fifth spot in 2Q21 due to services sales with domestic telcos. Cisco and Intel followed in the sixth and seventh spots, leveraging strength in the router market, and data centers and virtualization, respectively. CommScope, NEC, and Fiberhome round out the top 10. CommScope is a key provider in the connectivity market, both fixed and mobile, and for broadband CPE. NEC is becoming an important player in the emerging open RAN market. Fiberhome has a significant market share for network equipment in the Chinese telco market, across optical transport and mobile networks. Samsung, ranked 11 in 2Q21, is also a notable player in telco NI, as it is rising in the US due to success at Verizon, and has strong potential in Europe.

This telco NI market share study includes a wide range of vendor types and cuts across hardware, software, and services. If you consider only hardware & software revenues from one specific category of vendors, network equipment providers (NEPs), total revenues were $121.6 billion for the 2Q21 annualized period. The top ten providers for this market are Huawei, Nokia, Ericsson, ZTE, Intel, NEC, Cisco, Fiberhome, Samsung, and Fujitsu. The top 4 of these suppliers account for 64% of market revenues. This category (NEP hardware & software) most directly maps into what is sometimes reported as the “telecom equipment” market.

Winners and losers

On a USD basis, the biggest YoY Telco NI sales jumps in 1H21 were easily recorded by Ericsson and Nokia, up $1.46 and $1.01B respectively. Cisco, Samsung, and Dell Technologies (VMWare) also saw sizable growth in the telco vertical, as did several vendors riding China’s 5G boom: China Comservice, ZTE, and Fiberhome. On the downside, Huawei’s $1.48B YoY decline in Telco NI sales in 1H21 was far worse than any other supplier.

On a share change basis, Huawei again comes out at the bottom of the heap, comparing its annualized share in 2Q21 with that of 2Q20. As predicted, the company’s share of telco NI has now fallen below 20% (19.01% in 2Q21, annualized). Beyond Huawei’s special case, most changes are due to one of three factors: M&A, telco spending cycles, and technology dislocations. Recent M&A deals of note include Capgemini-Altran, CommScope-ARRIS, ECI-Ribbon, Hengtong-Huawei Marine, Casa-Netcomm, and Amdocs-Openet. A number of vendors have been impacted by telcos’ 5G infrastructure push, including the recent shift towards core network spending. Several large countries are seeing growth in fiber access deployment spending. Telcos’ increased adoption of the cloud in a variety of forms cuts across a large number of the changes seen in the below charts. AWS, Azure and GCP have all seen dramatic growth in their telco vertical revenues in the last few quarters, as has Dell Technologies (VMWare) and Arista. Regarding the share declines, Samsung’s annualized share change reflects a dropoff in Korean 5G spend as it still awaits a pickup in the US, India and/or Europe. Nokia’s share has stabilized, after falling due to a perception of falling behind in mobile RAN radio technology, as well as its backing away from China. Huawei’s share decline is due to political and supply chain obstacles.

Webscalers crash the telco party

Nearly a decade ago, as cloud services began gaining popularity, many telcos hoped to be direct beneficiaries on the revenue side. The cloud market went a much different direction, though, with large internet-based providers (aka webscalers) proving to have the global scale and deep pockets able to develop the market effectively. From 2011-2020 webscale operators invested over $700 billion in capex, a big portion of it devoted to building out their cloud infrastructure.

The cloud sector has geared its offerings to businesses of all stripes and sizes. Serving telecommunications operators was not an initial focus for many reasons. Telcos have unique network requirements and stringent reliability criteria, and tend to make purchasing decisions slowly. Many telcos also viewed cloud providers with trepidation, as potential competitors on the enterprise side. Yet the telecom market is also one of the biggest around, viewed as a prize worth fighting for. Nearly $300 billion in annual capex and $1.2 trillion in opex (excluding depreciation) are figures that are hard to ignore. Amazon Web Services (AWS) made the earliest strides in telecom, in 2015 (with Verizon), but Azure and GCP were serious about the market by 2017. Last year, Microsoft bolstered its 5G and cloud-based telecoms offerings with the big-ticket acquisitions of Affirmed Networks and Metaswitch Networks.

This telco-webscale collaboration activity has picked up in the last 12-18 months. Webscale operators help telcos with service and application development, shifting of workloads, and developing, enabling and marketing cloud-based services. Collaborations can involve delivery of a portfolio of 5G edge computing solutions that leverage the telco’s 5G network and the webscale operator’s global cloud coverage, as well as its expertise in areas like Kubernetes, AI/ML, and data analytics. Managing costs is a central purpose of telcos’ willingness to partner with webscale providers. Increasingly, the webscale operators who deliver cloud services are competing alongside traditional telco-facing vendors like Amdocs, Citrix, CSG and Nokia.

For the 4 quarters ended 2Q21, MTN Consulting estimates that AWS, Azure and GCP had aggregate revenues to the telco sector of $1.92 billion, up 78% from the 1Q20 annualized period. These cloud providers will sometimes be valuable partners for telco-focused vendors, but in many cases they will be competitors, and are important to track.

Optical, IP, and automation are hotspots after initial 5G builds

While Ericsson and Nokia have benefited from Huawei’s troubles, this displacement has not yet helped smaller vendors focused on areas like optical transmission and IP infrastructure. There is strong demand in these categories to support upgraded 5G radio and fiber access connectivity, but in 1H21 that mainly helped larger players who sell optics and IP infra as part of larger deals. For instance, Nokia’s 2Q21 optical sales to telcos were up 18% YoY to $403M, while Ciena and Infinera saw a 2% bump and 4% decline YoY in Telco NI, respectively. As telco spending picks up in core networks, smaller vendors aim to pick off more of Huawei’s business in the next 1-2 years. Infinera notes an “acceleration in the pace of Huawei replacement opportunities.” Ciena, ADVA, Ribbon, and Arista should also benefit.

Automation is another major investment theme in the telco market, cutting across many product segments. Orange, for instance, positions the automation of network management and maintenance as a central part of its “Scale-Up” operational efficiency program. Vendors highlighting automation in 2Q21 include Ciena, Cisco, DZS, F5, EXFO, Infinera, Juniper, Oracle, and many others. One illustrative win in 2Q21 comes from Amdocs, at T-Mobile: its “zero-touch service operations were recently selected for a program to implement next-generation automation, leveraging machine learning and AI tools.” This kind of win is important for Amdocs as it is one of many telco-focused vendors which face creeping competition from the cloud world.

Telco spending outlook for remainder of 2021

The telco industry put up big numbers in 1Q and 2Q 2021, but growth will slow in 2H. Telco industry capex is likely to come in around $300B for 2021, only slightly up from $295B in 2019. Telco opex budgets are a bit more appealing for vendors. Opex (excluding depreciation & amortization) is roughly 4x capex, and the network operations-related (“netops”) piece of opex is growing for many telcos. For 2021, MTN Consulting projects netops opex of about $297B, from $282B in 2020, and telco outsourcing of netops tasks are widespread and growing. Cloud providers are taking advantage of some of this growth, but a large number of traditional Telco NI vendors sell into telco opex budgets.

- Table of Contents

- Figures

- Coverage

- Visuals

Table of Contents

- ABSTRACT – Results commentary

- INTRODUCTION

- 2Q21 Telco NI Market Results

- TOP 25 VENDORS – Printable tearsheets

- CHARTS – Single vendor snapshot

- CHARTS – 5 vendor comparisons

- DATA – revenue estimates by company

- ABOUT – MTN Consulting and report methodology

Figures

Partial list:

- Telco NI vendor revenues, annualized (US$B)

- Telco NI revenues by company type, 2Q21 annualized

- Telco NI as share of total company revenues for top 25 vendors

- Telco NI as % of corporate revenues by company type

- Telco NI/Total

- Annualized Telco NI revenues vs. Capex and Opex (ex-D&A)

- Correlation between Telco NI revenues and Capex/Opex ex-D&A

- Annualized Telco NI vendor revenues ($B) vs. YoY growth in single quarter sales

- Telco NI sales of top 6 vendors vs. all others, 2Q21 TTM (annualized)

- Telco NI vendor revenues, YoY % growth in single quarter

- Top 25 vendors based on Telco NI revenues in 2Q21 ($B)

- Top 25 vendors based on annualized Telco NI revenues through 2Q21 ($B)

- Telco NI market share changes, 2Q21 v. 2Q20

- Top 25 vendors based on 2Q21 YoY revenue growth rate in Telco NI

- Top 25 vendors: results highlights and growth outlook

- Top 25 vendors in Telco NI Hardware/Software: Annualized 2Q21 Revenues (US$B)

- Top 25 vendors in Telco NI Services: Annualized 2Q21 Revenues (US$B)

Coverage

| Company | Segment |

| 3M | CCV |

| A10 Networks | NEP |

| Accenture plc | ITSP |

| Accton Technology | NEP |

| ADTRAN | NEP |

| ADVA Optical Networking | NEP |

| Affirmed Networks | NSP |

| Airspan | NEP |

| Alcatel-Lucent | NEP |

| Allied Telesis | NEP |

| Allot Communications | NEP |

| Altran Technologies | ITSP |

| Amdocs | ITSP |

| Anritsu | T&M |

| Arista Networks | NEP |

| ARRIS International | CCV |

| AsiaInfo Technologies | NSP |

| Atos Origin | ITSP |

| Audiocodes | NSP |

| Avaya | ITSP |

| Aviat Networks | NEP |

| AWS (Amazon Web Services) | NSP |

| Azure (Microsoft) | NSP |

| Beijing Xinwei | NEP |

| Broadcom Limited | NEP |

| BroadSoft, Inc. | NSP |

| Brocade Communications Systems, Inc. | NEP |

| CA Technologies | NSP |

| Calix | NEP |

| Capgemini | ITSP |

| Casa Systems | NEP |

| Ceragon Networks | NEP |

| Check Point Software | NSP |

| China Communications Services Corporation Limited | ES |

| Ciena Corporation | NEP |

| Cisco Systems | NEP |

| Citrix Systems | ITSP |

| Clearfield | CCV |

| Comarch | ITSP |

| Comba Telecom | NEP |

| CommScope Holding | CCV |

| Commvault Systems | ITSP |

| Comptel | NSP |

| Convergys | ITSP |

| Coriant | NEP |

| Corning | CCV |

| CSG | NSP |

| Cyan | NSP |

| DASAN Zhone | NEP |

| Datang Telecom Technology | NEP |

| Dell Technologies | NSP |

| DragonWave Inc. | NEP |

| DXC Technology (aka CSC) | ITSP |

| DyCom Industries | ES |

| ECI Telecom | NEP |

| Ericsson | NEP |

| EXFO Inc | T&M |

| Extreme Networks | NEP |

| F5 Networks | ITSP |

| Fiberhome | NEP |

| FireEye | NSP |

| Fortinet | ITSP |

| Fujikura | CCV |

| Fujitsu Limited | NEP |

| Furukawa Electric | CCV |

| General Cable | CCV |

| GCP (Google Cloud Platform) | NSP |

| Harmonic Inc. | NEP |

| HCL Technologies | ITSP |

| Hengtong Optic-electric | CCV |

| Hitachi | NEP |

| HPE | NEP |

| Huawei | NEP |

| Huber+suhner AG | CCV |

| IBM | ITSP |

| Infinera | NEP |

| Infosys | ITSP |

| Inseego | NEP |

| Intel | NEP |

| Italtel | NEP |

| ITOCHU Techno-Solutions Corporation | ES |

| Juniper Networks | NEP |

| Kathrein | CCV |

| Kudelski | NEP |

| MasTec | ES |

| Mavenir | NSP |

| Metaswitch | NSP |

| Mitsubishi Electric | NEP |

| NEC Corporation | NEP |

| Net Insight | NEP |

| Netcomm | NEP |

| NetScout Systems | NSP |

| Nexans | CCV |

| Nokia | NEP |

| Openet | NSP |

| OPTIVA | NSP |

| Oracle | NSP |

| Pace plc | NEP |

| Palo Alto Networks | NEP |

| Prysmian | CCV |

| Quantenna Communications | NEP |

| Radcom | NSP |

| Radisys | NSP |

| Radware | NEP |

| Red Hat | NSP |

| Ribbon Communications | NEP |

| Ruckus Wireless | NEP |

| Samsung Electronics | NEP |

| SAP SE | NSP |

| SeaChange International, Inc. | NSP |

| Sopra Steria | ITSP |

| Spirent Communications | T&M |

| Sterlite Technologies | CCV |

| Subex | NSP |

| Sumitomo Electric | NEP |

| SYNNEX Corporation | ITSP |

| Tata Consultancy Services | ITSP |

| TE Connectivity | CCV |

| Tech Mahindra | ITSP |

| Technicolor | NEP |

| Tejas Networks | NEP |

| Transmode | NEP |

| Trigiant Group | CCV |

| Virtusa | ITSP |

| Vubiquity | ITSP |

| Westell | CCV |

| Wipro | ITSP |

| Wiwynn | NEP |

| YOFC | CCV |

| ZTE | NEP |

Visuals