By Matt Walker

This commentary explains the network spending forecast update issued in August 2021, comparing it to the forecast published in December 2020 (“Network operator capex to hit $520B in 2025”). This forecast revision is modest: market dynamics are largely as we predicted in December 2020, and most projections are on track. However, some changes have occurred.

- Webscale continues to grow rapidly and record high profits. Webscalers are getting a boost from the lingering of COVID-19, with work and study from home becoming a long-term reality in many markets. Key cloud players are boosting capex outlook due to data center expansion, and also spending more rapidly on non-tech avenues like logistics and fulfillment. (See “Webscale Network Operators: 1Q21 Market Review”).

- There is strong private equity interest in the carrier-neutral sector, with a focus on data centers. We discuss this in our July 2021 report, “Tomorrow’s carrier-neutral operators to integrate tower, fiber and data center assets.” The increased PE interest in carrier-neutral models is enticing more telco asset spinoffs, including at Telefonica, Telstra, Singtel, PCCW, Indosat Ooredoo, PLDT, and Optus (some deals still under discussion).

- MTN Consulting has significantly expanded its coverage of software capex in the telco sector. Over the last 8 months, we have increased our sample size from 24 telcos to 63, and recalculated capex historically for all these providers. The result is twofold: one, a change in historic telco capex estimates (down for 2011-15, up for 2016-19); two, an improved estimate of software’s share of total capex in the telco sector. The trend in this metric is still positive, but at a more moderate clip.

- MTN Consulting has tweaked the Network/IT vs. All other capex splits for most key webscalers. The result is to decrease the Network/IT percentage of total. Both Network/IT and All other capex projections are up in this new forecast, but All other’s 2025 total is up by 35% while Network/IT is up by a more modest 15%. As webscalers use their cash and brands to expand, the tech spend piece gets a bit smaller as a share of total.

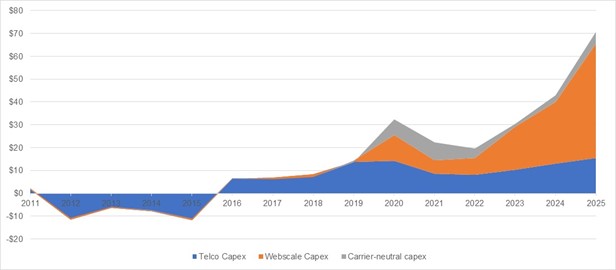

The 12/20 forecast called for total capex to climb from $425B in 2020 to $520B in 2025. The new forecast starts from a higher baseline, $457B in 2020, and grows to $591B in 2025. Webscale capex is slightly more important, accounting for 42% of 2025 capex from 39% in 2025 under the last forecast.

*

This product contains two files: a qualitative analytic report, and a detailed Excel file containing market size and spending estimates from 2011 through 2025 for the telecommunications, webscale, and carrier-neutral network operator segments.

- Table Of Contents

- Figures & Charts

- Coverage

- Visuals

Table Of Contents

Key sections include:

- Summary

- Telco Market Forecast

- Webscale Market Forecast

- Carrier-neutral Market Forecast

- Appendix 1: Additional Charts

- Appendix 2: About MTN Consulting

Figures & Charts

FIGURES

Figure 1: Capex by segment changes, 8/21 v. 12/20 forecast (US$B)

Figure 2: Telco capex by region and change from 12/20 forecast

Figure 3: Telco employees and average cost per employee ($K) through 2025

Figure 4: Software as % of total capex, telcos (August 2021 update)

Figure 5: Webscale capex by type: % change in forecast, 8/21 v. 12/20

Figure 6: New CNNO forecast compared to the 12/20 forecast

Figure A1: Capex by operator type ($B), August 2021 update

Figure A2: Capital intensity by operator type, 8/21 estimates

Figure A3: Webscale capex by type, 8/21 forecast update ($B)

Figure A4: CNNO data center footprint, net rentable square feet (M)

Coverage

This forecast report addresses three large segments of network operators, covering nearly 200 operators in total.

Specific companies or organizations mentioned in the report are as follows:

Alphabet

Amazon

Deutsche Telekom (DT)

Facebook

Indosat

Microsoft

Ooredoo

Optus

Orange

PCCW

PLDT

Singtel

Telefonica

Telstra

Vodafone

Visuals