By Arun Menon

This report reviews the growth and development of the telecommunications network operator (TNO, or telco) market. The report tracks a wide range of financial stats for 139 telcos across the globe, from 1Q11 through 2Q23. In the annualized 2Q23 period, telcos represented $1.76 trillion (T) in revenues (-5.1% YoY), $252.2 billion (B) in labor costs (-4.0% YoY), and $325.0B in capex (-2.0% YoY). They employed approximately 4.56 million people as of June 2023, down 1.2% from the prior year.

Telco revenues extend decline for seventh straight quarter, but pace slows

Telco revenues declined by 1.3% on a YoY basis to post $443.6 billion (B) in the three-month period covered by 2Q23 (April – June 2023). The quarterly dip was also the seventh consecutive slump. The pace of decline has decelerated though – the previous three quarters saw revenues sink by 6.3%, 9.3%, and 3.5% in 3Q22, 4Q22, and 1Q23, respectively. The waning effect of AT&T’s spinoff of its WarnerMedia unit coupled with improved service revenue growth for a large number of mobile operators played key roles in the market decline slowdown.

However, the sharp slides in the later half of the previous year coupled with declines in the first half this year impacted revenues and their growth rate for the annualized 2Q23 period – they were $1,757.9B, down 5.1% over the previous year. Currency fluctuations impacted many regions in the annualized 2Q23 period, but especially Japan: revenues for KDDI, Softbank, and NTT plummeted by 12.4%, 10.6%, and 8.8% YoY, respectively. Inflationary pressures and the energy crisis impacted European telco giants such as BT (-10.5%) and Vodafone (-8.4%).

Among the top 20 companies based on annualized 2Q23 revenues, Airtel saw the strongest growth in revenues, up 8.3%. The growth came on the back of rising ARPU and growing service subscriptions in its domestic market, as it begins a shift to 5G. Other telcos among the top 20 to post revenue growth in the annualized 2Q23 period include Saudi Telecom (6.5%), Charter Communications (2.6%), China Unicom (1.2%), Verizon (0.5%), China Telecom (0.3%), and China Mobile (0.2%). Notably, two of the big three Chinese telcos (China Mobile and China Telecom) witnessed revenue declines in the single quarter 2Q23, after staging a recovery in 1Q23. While the Chinese telcos attributed growth in the annualized period to a surge in their “emerging businesses” revenues, growth witnessed by some operators in less mature 5G markets was due more to 5G-related equipment revenues. Telcos are banking on 5G-enabled devices already deployed to potentially generate new revenue streams in the remainder of 2023 and beyond, but this seems unlikely. As such we expect telcos to be forced into major strategic changes and cost transformation programs in the near future. Recent success with opex cuts in delivering profit growth will embolden many telcos.

The worst annualized telco growth among the top 20 operators for the annualized 2Q23 period came from AT&T, down 23.9%, largely due to the effect of spinning off WarnerMedia in early 2022. However, 12 of the other top 20 operators posted a decline in revenues, without a big asset sale to explain the drop. Apart from KDDI and Softbank mentioned earlier, BT (-10.5%) was among the top 20 to post a >10% decline in revenues in the annualized 2Q23 period.

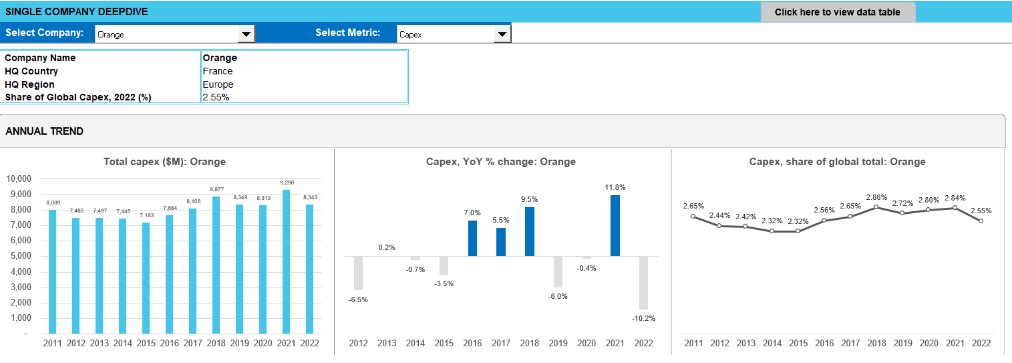

Capex records steepest decline since 2Q20 of 5.8% as 5G buildout pace moderates

Capex declined again in the latest single quarter after managing a recovery of sorts in 1Q23. Telcos in the US, China, and Europe are moving past peak 5G capital investment levels and are looking to bolster their finances amid declining top-line, macro pressures, and slowdown concerns. Capex declined by 5.8% on a YoY basis – the steepest fall since 2Q20 – to post $76.0B in 2Q23. The sharp decline in the latest quarter also knocked down the annualized capex, falling by 2.0% YoY to post $324.9B in 2Q23. This decline impacted annualized capital intensity which came off the highs from 18.7% in 1Q23 to total 18.5% in 2Q23; this ratio is still among the highest ever for the industry, however. Increased fiber roll-out and upgrade activities to support fixed broadband and to connect all the new radio infra (including small cells) needed for 5G, coupled with continued expansion of 5G in major markets like India, have aided annualized capital intensity to hover near record high levels.

At the operator level, Rakuten’s capital intensity exceeds all other telcos handily with a roughly 159.3% capex/revenue ratio for 2Q23, on an annualized basis. Rakuten’s ratio has been declining in recent quarters as its greenfield network rollout is reaching its peak. India’s state-owned telco, BSNL, recorded a capital intensity of 75.5% for the annualized 2Q23 period, as it prepares for phased roll out of 4G and 5G services this year. Frontier Communications’ capital intensity stood at 66.9% for the annualized 2Q23 period, driven by increased spending for fiber upgrades to its existing copper network and aided by government support for rural broadband. Reliance Jio’s capital intensity stood at 63.3% due to its aggressive target to roll out 5G pan-India by end of this year. Globe Telecom’s capital intensity for the annualized 2Q23 period stood at 49.8%, due to a network infrastructure buildup that includes building 542 new cell sites and upgrading 5,087 mobile sites to LTE across the country, alongside deploying approximately 148,000 fiber-to-the-home (FTTH) lines as of June 2023. Consolidated Communications and PLDT’s annualized capital intensity stood at 49.6% and 42.6%, respectively, in 2Q23.

The biggest capex spender in the annualized 2Q23 period was China Mobile ($25.1B), but this was down 14.3% from the annualized 2Q22 period due to tapered buildout pace and the telco’s efforts to share costs on the network side enabled by a partnership with China Broadcasting Network. Four out of the top 20 operators by capex spend posted double-digit growth rates for the annualized 2Q23 period. These include: Reliance Jio (72.6%), Airtel (38.2%), Charter Communications (33.1%), and Comcast (21.8%).

Telcos embrace digital transformation and technology-enabled solutions to boost profitability

Amid declining topline, telcos have historically managed to keep costs in check, allowing for stable profitability margins – EBIT margins have been in the range of 13-18% while average EBITDA margins have remained above 30% since 2011. The trend persisted into the annualized 2Q23 period despite the immense burden of investments, declining revenues, and macro pressures in the past several quarters. EBITDA margin for the industry was 34.8%, while EBIT (operating) margin stood at 15.6%, in the annualized 2Q23 period. Both figures are comfortably higher than two quarters ago. Within the overall telco opex budget, there is a noticeable trend of telcos effectively reducing their sales & marketing and G&A spending. This shift is a response to telcos adapting to remote work environments and accelerating the transition of sales and support functions to digital platforms. MTN Consulting anticipates that telcos will persist in reducing their workforce by modernizing their workflows, investing in digital transformation initiatives, and embracing automation. Meanwhile, many telcos are reporting that network operations is taking up a larger portion of the opex pie. To drive sweeping changes going forward, telcos will have to implement dramatic, strategic measures to optimize their cost structure in order to increase and sustain profitability. These strategic measures will be a mix of technology-enabled solutions and collaborations, some of which will transform the telco business model. While automation will continue to be a key enabler, other key strategic cost optimization measures that telcos will pursue over the next 2-3 years include core network sharing, network slicing, and partnerships with webscale cloud providers, each of which has the potential to hit multiple cost bases.

Telcos continue workforce reduction drive as the average telco employee turn costlier

Telco industry headcount was 4.56 million in 2Q23, down from 4.61 million a year ago. The declining trend in overall headcount was partially offset by increases at the largest three telcos in both China and India. MTN Consulting expects headcount reductions to continue via implementing automation, attrition, and voluntary retirement schemes, heading towards 4.17 million by 2027. Spending on employees (labor costs) on a per-person basis grew slightly to $55.1K in 2Q23 compared to $55.0K the prior quarter, as inflation has cooled and wage pressure from other sectors took a breather. However, rising living costs have increased demands for higher wages from employees in competitive labor markets. For instance, Telefonica agreed to raise 2023 wages for almost 13,000 workers in Spain amid high inflation. BT also agreed to a EUR1,500 pay rise for 85% of UK staff. In the US, Verizon, Charter Communications, and T-Mobile made headlines for boosting minimum wages of employees to $20 per hour. With these conditions likely to persist along with elevated demand for highly-skilled talent, the average employee will get costlier: labor cost per employee will likely hit $66.0K per year in 2027, from $55.1K in annualized 2Q23 period.

Asia beats Americas by revenues, but the latter outspends all other regions in capex terms

The Asia region managed to sustain its dominance in 2Q23 by a whisker, with 37.4% global share of the total telco market revenues versus 37.0% global share for the Americas region. In terms of growth, all regions except MEA registered revenue declines in 2Q23 with Asia declining the most by 2.4%. On a capex basis though, the Americas region continued to outspend the Asia region for the third straight quarter; US-based telcos such as Comcast, Charter Communications, and Frontier Communications are responsible for most of this growth. Asia registered a steep YoY decline in capex spend of 12.8% in 2Q23, thanks to reduced spending by the three Chinese telcos – China Mobile, China Telecom, and China Unicom. Chinese 5G capex is past its peak investment levels and there is a greater focus on network sharing. Europe continued its lead into the latest quarter for having the highest regional capital intensity on an annualized basis, with 19.7% in 2Q23, followed by Americas (18.9%). The Americas and Europe regions witnessed an uptick in annualized capital intensity this quarter when compared to 2Q22. Asia followed the Americas with annualized capital intensity of 17.9% in 2Q23 (vs. 18.6% in 2Q22), while MEA stood at 15.8%.

- Table Of Contents

- Figure & Charts

- Coverage

- Visuals

Table Of Contents

- Abstract

- Market snapshot

- Analysis

- Key stats through 2Q23

- Labor stats

- Operator rankings

- Company Deepdive & Benchmarking

- Country breakouts

- Country breakouts by company

- Regional breakouts

- Raw Data

- Subs & traffic

- Exchange rates

- Methodology & Scope

- About

Figure & Charts

- TNO market size & growth by: Revenues, Capex, Employees – 1Q20-2Q23

- Regional trends by: Revenues, Capex – 1Q20-2Q23

- Opex & Cost trends

- Labor cost trends: 1Q20-2Q23

- Profitability margin trends: 1Q20-2Q23

- Spending (opex, labor costs, capex): annual and quarterly trend

- Key ratios: annual and quarterly trend

- Workforce & productivity trends: 1Q14-2Q23

- Operator rankings by revenue and capex: latest single-quarter and annualized periods

- Top 20 TNOs by capital intensity: latest single-quarter and annualized periods

- Top 20 TNOs by employee base: latest single-quarter

- TNOs: YoY growth in single quarter revenues

- TNOs: Annualized capital intensity, 1Q16-2Q23

- TNOs: Revenue and RPE, annualized 1Q16-2Q23

- TNOs: Capex and capital intensity (annualized), 1Q16-2Q23

- TNOs: Total headcount trends, 1Q16-2Q23

- TNOs: Revenue and RPE trends, 2011-22

- TNOs: Capex and capital intensity, 2011-22 ($ Mn)

- TNOs: Capex and capital intensity, 1Q16-2Q23 ($ Mn)

- TNOs: Revenue and RPE trends, 1Q16-2Q23

- Top 79 TNOs by total opex, 2Q23

- Top 79 TNOs by labor costs, 2Q23

- TNOs: Software as % of total capex

- TNOs: Software & spectrum spend

- TNOs: Total M&A, spectrum and capex (excl. spectrum)

- Top 79 TNOs by total debt: 2011-22

- Top 79 TNOs by total net debt: 2011-22

- Top 79 TNOs by long term debt: 2011-22

- Top 79 TNOs by short term debt: 2011-22

- Top 79 TNOs by total cash and short term investments ($M): 2011-22

Coverage

Operator coverage:

| A1 Telekom Austria | Advanced Info Service (AIS) | Airtel | Altice Europe | Altice USA | America Movil | AT&T | Axiata | Axtel | Batelco |

| BCE | Bezeq Israel | Bouygues Telecom | BSNL | BT | Cable ONE, Inc. | Cablevision | Cell C | Cellcom Israel | CenturyLink |

| Cequel Communications | Charter Communications | China Broadcasting Network | China Mobile | China Telecom | China Unicom | Chunghwa Telecom | Cincinatti Bell | CK Hutchison | Clearwire |

| Cogeco | Com Hem Holding AB | Comcast | Consolidated Communications | Cyfrowy Polsat | DEN Networks Limited | Deutsche Telekom | Digi Communications | DirecTV | Dish Network |

| Dish TV India Limited | DNA Ltd. | Du | EE | Elisa | Entel | Etisalat | Fairpoint Communications | Far EasTone Telecommunications Co., Ltd. | Frontier Communications |

| Globe Telecom | Grupo Clarin | Grupo Televisa | Hathway Cable & Datacom Limited | Idea Cellular Limited | Iliad SA | KDDI | KPN | KT | Leap Wireless |

| LG Uplus | Liberty Global | M1 | Manitoba Telecom Services | Maroc Telecom | Maxis Berhad | Megafon | MetroPCS Communications | Millicom | Mobile Telesystems |

| MTN Group | MTNL | NTT | Oi | Omantel | Ono | Ooredoo | Orange | PCCW | PLDT |

| Proximus | Quebecor Telecommunications | Rakuten | Reliance Communications Limited | Reliance Jio | Rogers | Rostelecom | Safaricom Limited | Sasktel | Shaw |

| Singtel | SITI Networks Limited | SK Telecom | Sky plc | SmarTone | SoftBank | Spark New Zealand Limited | Sprint | StarHub | STC (Saudi Telecom) |

| SureWest Communications | Swisscom | Taiwan Mobile | Tata Communications | Tata Teleservices | TDC | TDS | Tele2 AB | Telecom Argentina | Telecom Egypt |

| Telecom Italia | Telefonica | Telekom Malaysia Berhad | Telenor | Telia | Telkom Indonesia | Telkom SA | Telstra | Telus | Thaicom |

| Time Warner | Time Warner Cable | TPG Telecom Limited | True Corp | Turk Telekom | Turkcell | Veon | Verizon | Virgin Media | Vivendi |

| Vodafone | Vodafone Idea Limited | VodafoneZiggo | Wind Tre | Windstream | Zain | Zain KSA | Ziggo | ||

| Masmovil |

Regional coverage:

| Asia | Americas | Europe | MEA |

Visuals