By Arun Menon

Telcos worldwide are finally getting onboard the 5G bus, delivering high speeds with low-latency and seamless experience to enterprises and consumers. The latest connectivity standard presents growth and monetization opportunities for telcos with new services targeting a wide range of vertical markets. However, telcos’ inability to convert these opportunities into major new revenue streams so far has held back industry growth.

One of the biggest concerns telcos face today is to keep profitability ticking amid the immense burden of investments, stagnating revenues, macro pressures worsened by Russia’s invasion of Ukraine, and fierce competition from new-age operators. The success of telcos in the 5G era will depend on unlocking value and efficiencies through cost optimization measures, thus ensuring a continuous flow of investments and profitability. This is not new for telcos, as they have been able to deliver steady profitability margins amid flat to slight revenue growth environments for the past several years. To do this, they resorted to traditional means of cutting costs in the past mitigation cycles, efforts which have been narrow and tactical in nature. These included asset sell-offs, real-estate rationalization, repair and maintenance outsourcing, shared services models, etc.

With uncertain macro-factors at play, telcos will find it much harder to optimize costs through traditional tactics alone. To drive sweeping changes going forward, telcos will have to implement dramatic, strategic measures to optimize their cost structure in order to increase and sustain profitability. These strategic measures will be a mix of technology-enabled solutions and collaborations, some of which will transform the telco business model. Each of the cost optimization measures target multiple cost centers to deliver savings. Listed below are five key strategic cost optimization measures telcos will implement over the next 2-3 years:

- Automation: Automation will be a key enabler to achieve savings in cost areas such as networks (through automated fault detection and self-optimization systems, for instance), energy (dynamic shutdown of unused network elements during idle time), sales and marketing (virtual assistants for customer support and experience), and G&A (admin tasks automation).

- Open RAN/vRAN: Telcos could explore reducing multiple cost bases using open interface-based technology solutions such as Open RAN and vRAN. These may offer reduced network-related costs such as infrastructure rentals, RAN power consumption, repair and maintenance, etc.

- Network sharing agreements: Telcos for many years have turned to sharing network elements among them primarily to save costs. The most common form of network sharing has been the joint use of cell sites, towers, backhaul transport networks, etc., called passive infrastructure sharing. This evolved to sharing of active network components in the recent years that includes RAN components and spectrum. To achieve further cost savings in the 5G era, telcos are exploring the sharing of core network components and functionalities (called “core network sharing”).

- Partnerships with webscale cloud providers: Through partnerships with cloud providers, telcos are reducing network costs by moving critical network functions and workloads to the cloud, saving energy costs by deploying custom-designed energy efficient hardware and architectures developed by cloud providers, and driving personalized marketing and customer experience by turning customer data into insights with cloud data and analytics.

- Network slicing: By segmenting parts of the network to cater to different customer types and use cases, network slicing will enable telcos to reduce opex costs through improved operations stemming from fewer cross-dependencies between network functions. This should also reduce maintenance costs as a result of isolated slices deployment, which shields disruptions in other part of the network.

While we expect these relatively new approaches to drive change going forward, telco cost mitigation will require a blend of traditional and broad strategic measures. The crux of any strategy will be to integrate or bring the various business functions closer instead of being siloed, to drive maximum cost efficiencies across the telco organization.

- Table Of Contents

- Figures

- Tables

- Coverage

- Visuals

Table Of Contents

Summary – page 2

Telcos wrestle to keep costs in check amid stalled growth and macro pressures – page 3

Managing opex efficiently requires dissecting it further into standardized cost categories – page 5

For telcos, network-related costs alone account for ~50% of total opex – page 7

Group-wide efficiencies will depend on the control of overhead costs beyond networks – page 9

Telco labor costs are on the rise despite industry headcount reductions – page 12

New technology and partnerships are key tenets of telco cost savings in the 5G era – page 14

Traditional cost-saving measures continue – page 19

The mix of newer, more strategic cost cutting efforts and traditional approaches will vary with the operating climate – page 20

About – page 21

Figures

Figure 1: Operating margins: Global telco market, annual

Figure 2: Global telco revenue, YoY growth rate (%)

Figure 3: Telco capital intensity (Capex/Revenues), annualized

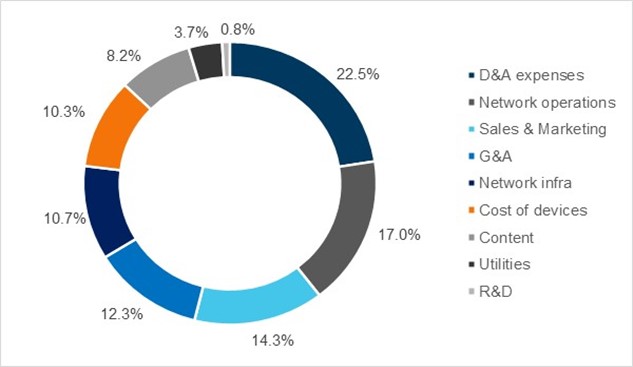

Figure 4: Opex items as a % of total opex, group of 30 telcos: Average, 2016-21

Figure 5: All network-related* opex, % total opex: Group of 30 telcos

Figure 6: Network-related opex categories as % of total opex: Group of 30 telcos

Figure 7: Telco-specific opex (non-network) as % of total opex: Group of 30 telcos

Figure 8: Non-telco-specific costs as % of total opex: Group of 30 telcos

Figure 9: Labor costs as a % of total opex: Group of 30 telcos

Figure 10: Labor costs per employee (US$K): Group of 30 telcos

Tables

Table 1: Automation’s impact on opex by cost area

Table 2: Network slicing’s impact on network operations opex

Table 3: Open RAN and vRAN impact on opex by cost area

Table 4: Network sharing impact on opex by cost area

Table 5: Cloud partnerships’ impact on opex by cost area

Coverage

Companies and organizations mentioned in this report include:

1&1 AG

Amazon

AT&T

Bharti Airtel

Bouygues Telecom

BT

Charter Communications

China Telecom

China Unicom

Comcast

Deutsche Telekom

Dish Network

Du

Ericsson

Etisalat

Globe Telecom

KDDI

KT

Microsoft

MTN

Netflix

Nokia

Ooredoo

Orange

Rakuten Mobile

Reliance Jio

ServiceNow

SK Telecom

Telecom Italia

Telefonica

Telenor

Telia

Telkom Indonesia

Telus

Turkcell

Verizon

Vodafone

Visuals