|

|

|

|

Webscalers ramp up push into telecom in 1Q21

|

MTN Consulting's formal review of 4Q20 performance for the webscale sector will be published within a week. Based on preliminary stats, it is clear that the webscale market of operators continued blockbuster growth in 2020, ending the year with just over $1.7 trillion in revenues, from $1.45T in 2019. The growth is due to several factors: acquisitions (e.g. Alibaba-Sun Art, Amazon-Zoox, and Microsoft-Zenimax); strong digital advertising spend (e.g. Google up 9% YoY to $146.9B), and increased cloud spending across a number of verticals amidst the COVID-19 pandemic.

|

Webscalers have been attacking the telco vertical for several years. Since the close of 4Q20, over the last three months the webscale sector's efforts to engage telcos have picked up steam. A number of telcos have recently announced new deals with webscalers in the areas of edge computing, service development, digital transformation, and workload shift. At the same time, more traditional suppliers to telcos (e.g. Nokia) have expanded their own collaboration with the cloud providers who dominate the webscale market. These deals aim to differentiate among traditional telco vendors, prevent webscalers growing too fast in the market, and save costs for telcos. What follows is a brief outline of some of the key developments in 1Q21.

|

Telco deals with webscalers

|

Key deals from 1Q21 include the following.

|

Telefonica has engaged IBM, classified as a webscale operator in our coverage, to act as a systems integrator for an open RAN trial in Argentina. The proof of concept includes software and hardware components from Altiostar, Red Hat (an IBM subsidiary), Quanta, Gigatera, and Kontron. SDx Central notes that the trial follows on recent work between IBM and Telefonica on an overhaul of the telco's enterprise-focused cloud platform ("Cloud Garden 2.0")

|

|

TIM Brasil announced it would work with Oracle and Microsoft to migrate all of its on-premises workloads to the cloud. Capacity Media notes that the telco will "leverage Oracle Cloud Infrastructure (OCI) and Microsoft Azure, to move its mission-critical applications to the cloud, optimising and simplifying management of its IT infrastructure, as well as improving scalability and agility."

|

SK Telecom made several announcements in 1Q21:

|

- The company will connect its 5G mobile edge computing services with 34 other telcos across multiple regions via the Bridge Alliance.

- With Dell Technologies and its subsidiary VMWare, SK Telecom will create a technology called OneBox MEC to combine private wireless capabilities with an edge computing platform.

- In early January, the Korean telco announced the launch of SKT 5GX Edge in collaboration with Amazon Web Services. The service allows its customers to build mobile applications that require ultra-low latency, according to Capacity Media.

South African provider Vodacom Business announced that it was certified as "the first" AWS partner in Africa to attain the AWS Outposts Ready designation. Vodacom clients can purchase datacenter managed services from both Vodacom and AWS, choosing a mix of private cloud on-premises, Vodacom data center hosting, public cloud using a local AWS availability zone, or a combination of multiple options.

|

Telecom Egypt has selected IBM and its Red Hat unit to develop an open hybrid cloud strategy. Per Computer Weekly, the largest telco in Egypt "has implemented IBM Cloud Pak for Automation to infuse artificial intelligence (AI) into its workflows to provide the flexibility to scale automation projects quickly, across any cloud or on-premise environment."

|

Google Cloud announced a win at Canada's Telus billed as a 10-year strategic alliance. The two will co-develop "new services and solutions that support digital transformation within key industries, including communications technology, healthcare, agriculture, security, and connected home." The collaboration will also target network modernization within Telus' operations. Telus will use GCP's managed application platform, Anthos, to support 5G services and mobile edge computing.

|

Singtel announced it would offer 5G edge computing over the Microsoft Azure cloud platform. Trials will start later this year, and ultimately allow Singtel clients to run applications such as autonomous vehicles, drones, robots, and VR/AR with very low latency.

|

Australia's Optus, a unit of Singtel, signed a 3-year partnership with Google Cloud to transform its customer support operations, using GCP's Contact Center AI solution.

|

Globe Telecom in the Philippines announced it would use AWS to accelerate its own digital transformation and improve customer experience. Per the Manila Standard, Globe has "migrated carrier-grade and mission-critical applications, including contact center operations, customer analytics, network and service assurance systems and infrastructure operations, monitoring, and security, from its on-premises data centers to AWS." That includes transitioning 3,000 customer service agents from a legacy Avaya solution to Amazon Connect.

|

Liberty Global's Belgium unit, Telenet, announced vendors for its 5G rollout in March which include Ericsson, Nokia and Google Cloud. Ericsson won the radio access, and Nokia the core. Nokia will leverage Google Cloud's Anthos for Telecom platform in Telenet data centers. Liberty says the Anthos platform will provide "the innovation infrastructure with solutions and applications for 5G users, to drive better customer experiences and service."

|

Telecom-focused vendors partnering with cloud providers

|

Nokia was by far the most active of telco-focused vendors in 1Q21, announcing several collaborations with the webscale sector.

|

In January, Nokia announced a partnership with GCP to develop cloud-native 5G core solutions. Nokia is supplying its voice core, cloud packet core, network exposure function, data management, and 5G core, while GCP's Anthos for Telecom platform will serve as the platform for deploying applications. In March, Nokia expanded its work with GCP, announcing it would also partner to develop cloud-based 5G radio solutions. The collaboration leverages Nokia's RAN, Open RAN, Cloud vRAN and edge cloud technologies with GCP's edge computing platform and application ecosystem. Initial efforts center around Cloud RAN, and aim at integrating Nokia's 5G virtualized distributed unit and virtualized centralized unit with Google's edge computing platform running on Anthos. Nokia aims to certify its AirFrame Open Edge hardware with Anthos.

|

At the same time as the March GCP announcement, Nokia announced deals with Microsoft and Amazon.

|

The Microsoft agreement will develop "new market-ready 4G and 5G private wireless use cases designed for enterprises", combing Nokia's Cloud RAN, Open RAN, radio access controller, and multi-access edge cloud technologies with the Azure Private Edge Zone.

|

With Amazon Web Services, Nokia and AWS will conduct joint R&D into enabling Nokia's RAN, Open RAN, Cloud RAN, and edge solutions to operate "seamlessly" with AWS Outposts. The goal is to develop new customer-focused 5G solutions. Per Nokia, "operators will be able to simplify the network virtualization and platform layers for the Core and RAN network functions by leveraging the agility and scalability of cloud." Ultimately Nokia will be able to leverage Amazon services like EC2, EKS, Local Zones and others to help automate network functions and deploy end customer applications.

|

Intel, which has attacked the telco market aggressively over the last few quarters, signed a deal with GCP in February to develop "reference architectures and integrated solutions" for telcos to enable 5G and edge network solutions. The collaboration involves three main aspects: virtualized RAN and open RAN solution development; a network functions validation lab; and, service delivery to the edge.

|

Israeli telco vendor Radcom announced the integration of its 5G assurance solution (ACE) with Microsoft Azure. Radcom says that the integration of ACE with Azure "enables operators to assure the quality of 5G services by leveraging AI and machine learning-driven assurance and automation" ACE runs as a cloud native function over the Azure Kubernetes Service.

|

|

Vendor collaborations with webscalers will continue throughout 2021, no doubt. Mavenir's SVP for Business Development, John Baker, addressed this trend indirectly in a January interview with SDx Central: “I really do believe the hyperscalers are going to become the new telecom providers going forward...Apart from the physical radio that goes on a tower, everything we’re doing now follows the data center model, and these guys know how to manage data centers, software, and applications."

|

|

|

|

|

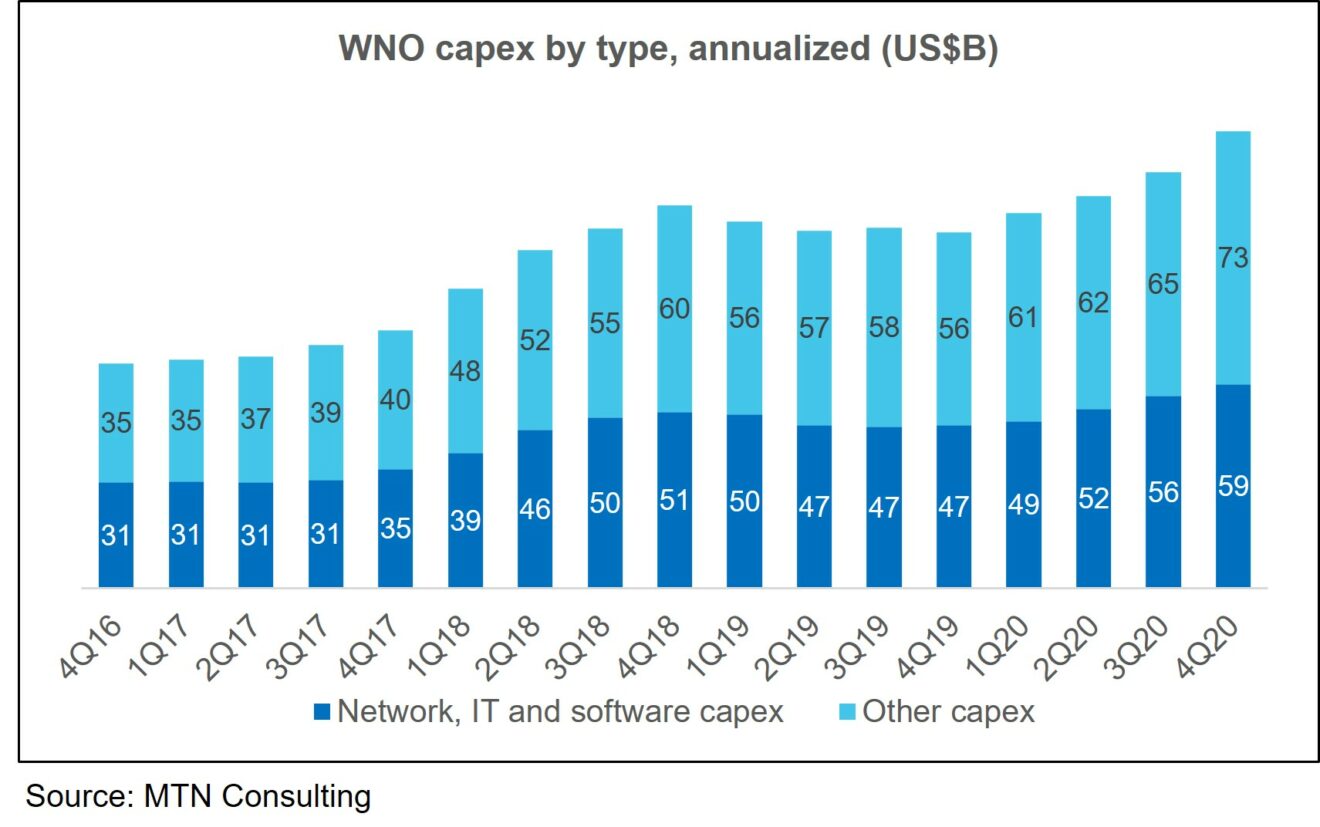

For webscale operators to support all these new activities requires heavy investment in network infrastructure. The figure below shows capex by type, on an annualized basis, for the total webscale network operator market since 2016.

|

|

|

|

Contact us for more information about our 4Q20 webscale market review.

|

|

|

|

MTN Consulting: Company news

|

Recently published reports

|

|

Telco Capex: 4Q20 Results & Outlook

|

Network spending proves resilient amidst COVID-19 pandemic as capex falls modestly, down 1.8% in 2020 to $294 billion; 4Q20 capex climbed 1.2% YoY

|

Published March 30, this report is currently available for sale on our website. A capsule summary follows:

|

|

|

"The global telecom industry bounced back in 4Q20 with 3.4% and 1.2% YoY growth in revenues and capex, respectively. Revenues for CY2020 declined 1.1% to $1.794 trillion. This is not exactly a sign of 5G stimulating market demand, but reassuring relative to the 5.4% YoY revenue decline recorded during the worst quarter of the pandemic’s spread, 2Q20. Total industry capex for 2020 was $294.1 billion, down 1.8% YoY, due in part to a 7.3% surge in China as a government push accelerated 5G rollouts. Japan was also a highlight due to Rakuten, NTT and KDDI. The biggest capex declines in 2020 occurred at AT&T, Jio, America Movil, Telefonica, and Vodafone Idea. The reductions at Jio and VI illustrate a common telco predicament: the need to restrain network capex to cope with expensive spectrum costs.

The relationship between capex and revenues in the telecom industry has stabilized, with annualized capital intensity remaining in a narrow window around 16.5% for several years. 2020’s figure was 16.4%. This outperforms the 16.0% MTN Consulting expected for 2020, but we still expect average capex/revenues to glide towards the 15% range by 2025. That is just an average; individual telcos continue to record a wide range of capital intensity metrics, from the low single digits to an extreme of 148.2%, for Rakuten.

In the M&A world, the biggest industry change in 2020 was the completion of Deutsche Telekom’s acquisition of Sprint. This has pushed DT into a leadership position in the industry, as it recorded $6.5B in 4Q20 capex, exceeding even China Mobile’s second-ranked $6.0B. Expect DT to exert a stronger influence on industry standards and vendors’ product decisions going forward. Also, the company’s now larger exposure to the US market will tend to make it more sympathetic to the growing global reluctance to use Chinese vendors’ gear. After DT and CM, the biggest spenders in terms of 4Q20 capex were AT&T, NTT, Verizon, China Telecom, Comcast, Vodafone, Orange, and China Unicom. This pecking order is largely unchanged from recent periods, where the top few operators in the US, China, and Europe dominate rankings.

Relative to company size, the biggest spenders among major telcos in 4Q20 were Telecom Italia, Veon, Rostelecom, Ooredoo, CK Hutchison, and Iliad. All recorded capital intensity above 30% on a single quarter basis. The transition to 5G is not the only factor. Costly fiber deployments were an issue for Iliad and Telecom Italia. Veon spent heavily on scaling up 4G across its footprint. Rostelecom’s core capex is supplemented by state program investments; the company’s share capital is 38% owned by the Federal Agency for State Property Management. For Ooredoo and CK Hutchison, 5G was the main driver; CK Hutchison has already made adjustments to its capex burden by agreeing to sell its European towers to Cellnex. One cost driver for many of the big telcos with high capex burdens is the growing cost of developing and/or acquiring software. MTN Consulting expects software to account for a rising percentage of overall network investments over the next few years.

For 2021 we maintain our current outlook: $1,791B in revenues and $292B in capex for the telecom industry, for an average capital intensity of 16.3%. Capex may trend to the high side of this target, however. One uncertainty around our 2021 capex forecast..." READ MORE

|

|

|

Biden aims to revamp US chip & telecom prowess amid China conflict

|

Activist approach aims at communications network supply chains and semiconductor development; bipartisanship appears feasible

|

Published March 19, this report lays out the likely approach the Biden administration will take with regards to Chinese telecom supply chains and the US semiconductor industry. A summary follows:

|

|

|

"The November 2020 election of Joe Biden to become the 46th President of the United States is having a number of sweeping effects. The most crucial one relates to the COVID-19 pandemic: Biden’s team has changed both tone and policy, and launched an aggressive, coordinated rollout of vaccines across the US population. Biden’s election will also have important impacts on communications network infrastructure markets, in at least two important ways.

First, US policy will continue to restrict much of the Chinese technology sector’s access to US supply chains; the US government will aim to minimize deployment of Chinese technology in both US communications networks and those in allied countries; and, US policy will support alternative technologies and companies that can help smooth the transition away from China. Implications: Huawei will see market share in the telecom sector decline markedly over the next 2 years; China will push harder on its own allies to purchase Huawei/ZTE gear; Huawei and ZTE will emphasize services and software more, and hardware less; China will explore many ways around the rules but see limited success without crucial chipmaking technology; Open RAN will see an accelerated adoption curve; US companies like Ciena, Cisco, and Infinera, and others (e.g. Fujitsu and NEC), will see telecom opportunities pick up significantly in 2H21 and 2022.

Second, the US will actively support the development of a semiconductor supply chain with more firm roots in the US mainland, and also aim to offset the growing global dependence on a single contract manufacturer (foundry), Taiwan-based TSMC. Implications: China will accelerate development of its own chipmaking industry and simultaneously use all means of political persuasion and bullying to bypass supply chain restrictions; Chinese hacking of the semiconductor sector will be more vigorous and aggressive than usual, both aimed at theft and at sabotage; China’s threats to invade Taiwan will get increasingly boisterous..." READ MORE

|

|

MTN Consulting's planned reports for the next few weeks include the following:

|

- Network Spending Profile: Orange

- Webscale Network Operators: 4Q20 Market Review

- 360 CI: Data Center Chips

- Telecom Network Operators: 4Q20 Market Review

|

|

|

To see our most recently published reports, click here

For information on subscribing to our research services, click here

|

|

You are receiving this because you are signed up to receive MTN Consulting's latest blogs and research alerts. We hope you enjoy our content, but you can unsubscribe at any time with the link at the bottom of this email - or by replying with "unsubscribe".

|

|

|

|

|

|

|