|

|

|

|

|

|

MTN Consulting will be releasing its annual forecast of network operator capex next week. The scope spans the telecom, webscale and carrier-neutral network operator markets. I am happy to share an early look with our loyal subscribers. Below please find the scene-setting introduction to the report, with a summary of revenue and capex projections. As this report is still in production, we would welcome any feedback.

|

Once published, the report will be made available immediately to subscribers, and also available for sale on our website.

|

Best regards,

Matt Walker

Chief Analyst

|

|

|

|

_____________________________________________________________________

|

"NETWORK OPERATOR CAPEX TO HIT $520B IN 2025" - early look at upcoming report

|

Telcos to save themselves by leaning on webscale & carrier-neutral sector

|

For many years the telco sector has enviously observed the dramatic growth of webscale network operators (WNOs) like Alphabet, Facebook and Microsoft. WNOs have grown quickly and maintained high levels of profitability, and are now among the biggest few companies on public stock exchanges. Meanwhile the telco sector has been flat, and achieving its much lower margins has required major changes in organization and processes. Weak top-line growth has enticed telcos to spin off assets and lease more of their infrastructure, leading to the growth of carrier-neutral network operators (CNNOs). In 2020, COVID-19 accelerated the shift of users and traffic towards the cloud services run by the webscale sector, and many telcos are ramping up their efforts to spin off passive infrastructure such as cell towers.

|

Will 5G somehow change the trajectory of the telecom industry? Despite the hype, the answer is no. Deploying 5G-reliant services will be costly both on the network and operational side. Mass market 5G services will not suddenly cause revenues to spike, and that is a view supported by early deployments. Niche 5G rollouts aimed at specific verticals or large enterprises have promise but will also be expensive to support, and do not fit easily into the telco operational model.

|

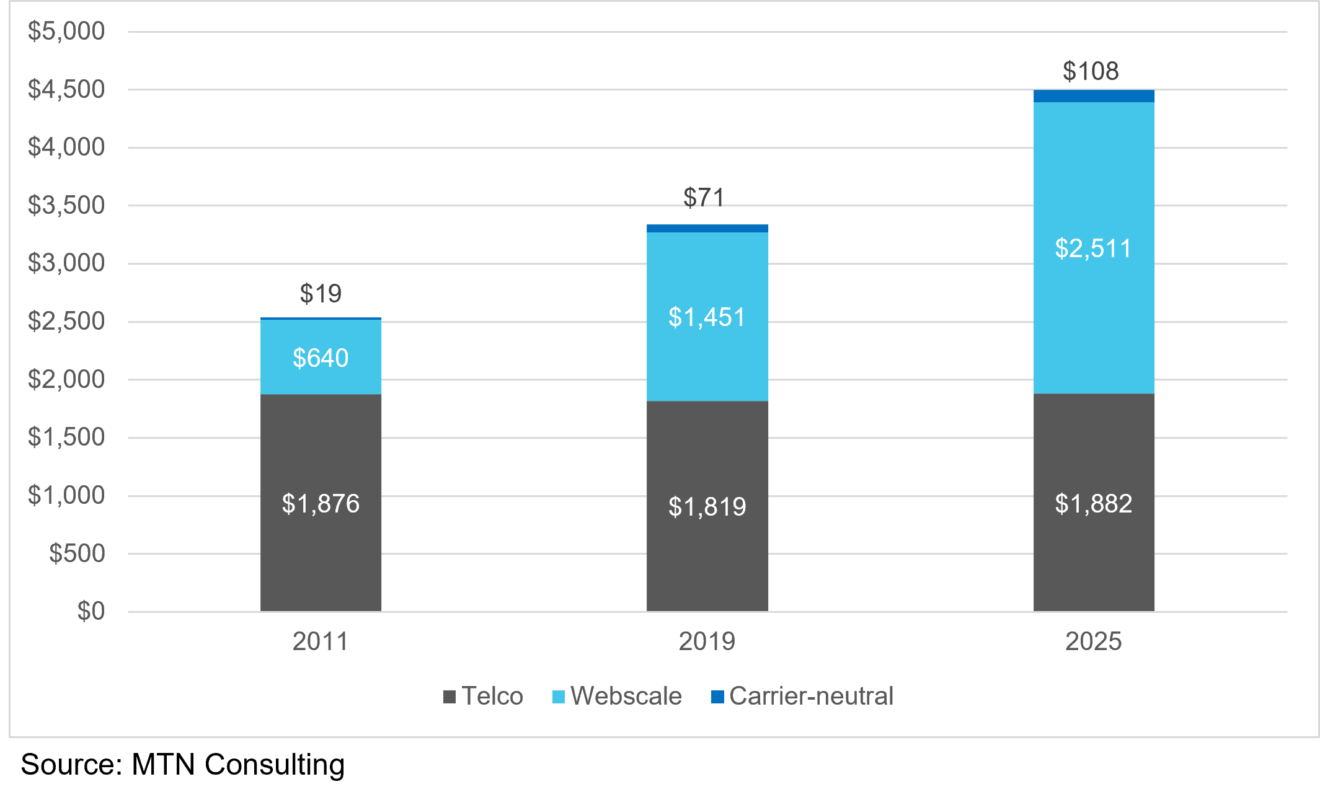

Figure 1 summarizes revenues by sector, showing 2011 and 2019 actuals and 2025 forecast figures.

|

|

Figure 1: Revenue prospects for telecom, webscale and carrier-neutral sectors (US$B)

|

|

|

However, telcos do have a saving grace. While many observers – including more than a few telco execs – look at the webscale sector with trepidation, the smart ones are now pursuing collaboration. A wave of promising partnerships between telcos and webscale providers has emerged over the last 12-18 months. Telcos are relying on webscale providers to shift workloads, such as core cloud capacity, but also more sophisticated tasks as service development and functionality. Telcos are also lowering their network construction cost needs by renting raw tower, fiber, and data center space from CNNOs.

|

To the webscale sector, the telecom industry is more than just another vertical market. Microsoft’s 2020 acquisitions of Affirmed and Metaswitch made that clear. Webscale providers need technology from the telco to bridge the last mile, support customers on their clouds, and to enable new 5G-based IoT services. It’s true that nearly all big webscale players are investing in satellite networks for communications capability, but the satellite option is a complement to telco networks, not a substitute. Cost and performance in the satellite world remain uncompetitive with telco alternatives. With telco networks taking decades to build, the webscale and telco sectors are stuck with each other.

|

Making money from tech: telcos to remain focused on cost reduction

|

Which brings us to a crucial distinction between telco and webscale. There are basically two ways to make money in the tech industry. One, use technology to change user behavior, creating demand for new ways of doing things and entirely new classes of products. Two, use technology to lower your cost of production, so the gap between your top and bottom line grows over time. Webscale operators are doing both simultaneously: investing heavily in R&D to create entirely new services and markets, while also continually leveraging their scale to lower production costs. For telcos, though, their success hinges on option 2: cost reduction.

|

Telcos’ necessary emphasis on option 2 will have a big impact on how their networks are built and operated over the next five years, and on which vendors benefit. We discussed these trends in our early 2020 reports on software and automation. Software is rising as a percent of total telco capex, and that will continue. Telcos are revamping operations in order to automate whatever they can, relying both on software from traditional telco vendors and partnerships with the webscale sector. Layoffs in the industry will accelerate, but so will hiring more costly engineers with software development skills. The most expensive part of the network, the mobile RAN, will continue its gradual shift towards disaggregation. That will create new opportunities for small vendors but also create demand for integrators and support the telco trend towards consolidation.

|

On the webscale side, their R&D operations are so big now that they buy very little gear off the shelf from traditional vendors, instead preferring to design things to spec and procure directly from ODMs – or simply acquire promising sources of new tech. Big opportunities still exist for vendors in the webscale world, but they must craft their positioning with an understanding that vendors would prefer to bypass them completely, and have the cash to do so. To date, vendors of transmission, IP infrastructure, chips, and basic connectivity (e.g. fiber, power) products have benefited, but don’t be surprised to see (more) webscale acquisitions in these sectors over the next few years.

|

Carrier-neutral providers will continue growth largely through acquisition of existing assets, but also invest capex in new areas such as mobile small cells, niche fiber routes, and helping smaller webscale players build out their clouds.

|

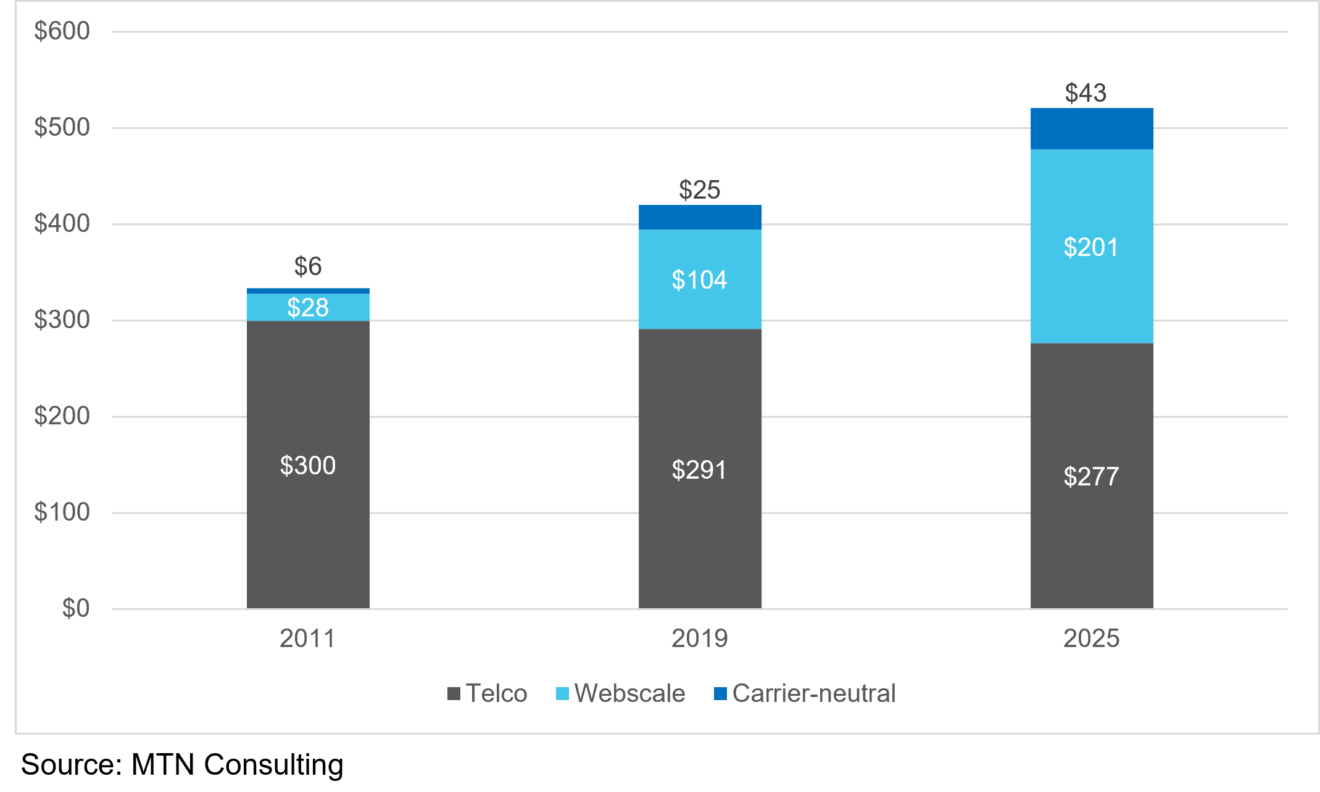

Figure 2 summarizes capex by sector, showing 2011 and 2019 actuals and 2025 forecast figures.

|

|

Figure 2: Capex prospects for telco, webscale and carrier-neutral sectors (US$B)

|

|

|

|

This report presents MTN Consulting’s first annual forecast of network operator capex. The scope includes telecommunications, webscale and carrier-neutral network operators. The forecast presents revenue, capex and employee figures for each market, both historical and projected, and discusses the likely evolution of the three sectors through 2025. In the discussion of the individual sectors, some additional data series are projected and analyzed; for example, network operations opex in the telco sector. The forecast report presents a baseline, most likely case of industry growth, taking into account the significant upheaval in communication markets experienced during 2020. Based on our analysis, we project that total network operator capex will grow from $420 billion in 2020 to $520 billion in 2025, driven by substantial gains in the webscale and (much less so) carrier-neutral segments. The primary audience for the report is technology vendors, with telcos and webscale/cloud operators a secondary audience.

|

|

|

____________________________________________________________________

|

RECENTLY PUBLISHED RESEARCH

|

In the last few weeks, MTN Consulting has published the following reports as part of our annual subscription service, "Global Network Infrastructure":

|

The purpose of this report is to provide a compilation of demographic, economic and telecommunications statistics for a large number of countries (167) in a user-friendly format... CONTINUE READING

|

After years of delay with 10nm chips, production roadblocks are again haunting Intel. The company has confirmed that its new line of server processors and chips based on 7nm process nodes have been delayed until 2022. The setback has sent Intel into a tizzy as rivals see a rare chance to knock Intel off its perch. On the rivals’ radar is the high-margin data center (DC) chips market, which is often touted as Intel’s “crown jewel,” as its market share is over 90 percent.

|

Hard-pressed by the current production upheaval, a combination of internal and external factors is expected to dent Intel’s share of the DC chips pie. Among the factors impacting Intel, the most obvious is the increased competition from rivals across the value chain which includes fabless chipmakers (AMD, Nvidia), pure-play design houses (Arm), and foundries/fabs (TSMC, Samsung). There is also a big in-house problem – Intel’s R&D, which previously failed to keep up with the standard two-year time frame to develop a new chip under “Moore’s Law”, is now battling with the current three-element process cycle that usually follows a three-year timeframe. In the medium-to-long run, several other factors — such as backward integration of webscalers, China’s self-sufficiency drive in semiconductors, and the emergence of open-source architecture such as RISC-V — are threatening to cut into Intel’s forte in the DC realm.

|

To sustain its market leadership in the DC chips market, Intel needs...CONTINUE READING

|

Annualized capex fell to $285.6B in 2Q20, as COVID-19 encourages cost cutting and procrastination; the new normal favors software and automation

|

Webscale capex hit an all-time high in 2Q20, but the opposite happened in telecom. Telco capex in 2Q20 amounted to $65.5B, down 6.2% from the 2Q19 period. That pushed telco capex on an annualized basis down to $285.6 billion, the lowest point in at least a decade. Vendors selling into the telecom sector felt this pain. Setting aside Huawei, whose 2Q20 revenues soared on the back of Chinese 5G builds, the rest of the vendor industry saw telco sales drop 5.3% in 2Q20.

|

The spread of COVID-19 has caused massive economic dislocations across the world, and the telecom sector was not immune. However, in profitability terms, 2Q20 was a good quarter for telcos, just as it was for the webscale players. While negative growth rates were the norm in 2Q20 for telecom, the bottom line wasn’t all that bad. Estimated EBITDA for the telco sector fell 2.8% in 2Q20 YoY, and EBIT dropped 4.1% on average. Since revenues declined at the faster 5.4% clip in 2Q20 on a YoY basis, overall margins improved on both an EBITDA and EBIT basis. Some of the margin improvement is due to telcos’ leveraging demand growth for fixed broadband and services aimed at remote workers. Many telcos reported improvements in their fixed line operations, with Telecom Italia noting an “inversion” in the fixed to mobile substitution effect. However, as noted, overall revenues did fall 5.4% YoY, so profit growth was more about cost control.

|

Reduced headcount is one possible explanation. Telcos employed 5.11 million at the end of June 2020, from 5.21 million a year earlier. Earnings reports show, however, that labor costs rose again in 2Q20, on a relative basis: from 23.5% in 2Q19, labor costs were 24.3% of opex (ex-D&A) on an annualized basis in 2Q20. Many telcos pointed to reductions in marketing expenses, as demand for new services slowed to a halt. They also cited...CONTINUE READING

|

Telco NI vendor revenues decline by 5% YoY in 2Q20 for market excluding Huawei, which surged amidst China's 5G push

|

Vendors signal a weak 2H in telco market after another YoY decline in 2Q20; China boosts Huawei

|

Vendor revenues in the telco network infrastructure (telco NI) market declined again in 2Q20 on a year-over-year (YoY) basis, for the third straight quarter. Huawei’s unusual first half report skewed the market upwards, to produce a global average decline of just 1% YoY. However, if you exclude Huawei, the rest of the telco NI market dropped by a steeper 5.3%. Removing both ZTE and Huawei would yield a telco NI decline of 6.3%. Telco spending stats are consistent with this steep drop, and not surprising given the economic pressures induced by COVID-19.

|

The Chinese government’s decision to step on the 5G accelerator lifted global averages, and it also lifted Huawei’s fortunes. Huawei has a huge embedded base of equipment across the globe, true, but large telcos in a wide range of developed and developing markets are turning away from the vendor as they make their 5G decisions. Since the arrest of Huawei’s CFO in December 2018, longstanding concerns about the company’s close links to the government have come out of the shadows. This has given a boost to its rivals across the board, and in the mobile RAN has spurred more telco interest in open RAN.

|

China’s 5G base station count surges in 2Q

|

Vendor revenues in the telco NI market have been flat for several years, hovering between $210 and $220 billion on an annualized (12 month rolling) basis. Telco spending – both capex and network opex – has followed a similar pattern of limited volatility. Network build cycles come and go at different times across the globe. Even with generational upgrades like 3G to 4G in the mobile RAN, the spending doesn’t happen all at once. China is the exception. Its telecom industry plays a big part in the government’s overall industrial policy, and all key operators are state-controlled through shareholding and other means. Hence, when the Chinese government decides to make a push, global market stats can be affected in a big way. That happened in 2Q20.

|

For all reporting vendors, telco NI revenues in 2Q20 amounted to $53.6B, down 1% from 2Q20. That’s an improvement from consecutive 5% declines in 4Q19 and 1Q20. But the improvement is due mainly to Huawei and ZTE, whose telco NI revenues rose 16 and 11%, respectively, from 2Q19 (in USD terms). Their growth stems from a surge in 5G base station spending in China. The government wanted to establish perceived “leadership” in 5G, stimulate a sagging economy, and help out national champion Huawei as its global fortunes sagged. Based on MIIT data, China had a total of 130,000 5G enabled base stations at year-end 2019, added 68K in 1Q20 and another 212K in 2Q20. That means about 75% of the newly built (or upgraded) 5G base stations in 1H20 were completed in the second quarter, in line with Huawei’s surge.

|

Relying exclusively on Chinese government (e.g. MIIT) stats in support of an argument is always risky. However, Ericsson also points to a 2Q20 surge in China 5G spend. Ericsson has pushed for a position in China’s 5G rollouts for many years, and that apparently hit in 2Q: China was 4% of Ericsson’s reported revenues in 1Q20, but 9% in 2Q20.

|

Strangely, China Comservice’s 1H20 report was a disappointment, with telco revenues down 12% YoY. The company points to delayed 5G decisions in China, but this doesn’t match other datapoints from China. It’s likely that Huawei and ZTE have been doing lots of turnkey 5G upgrades with services included, crowding out (for now) China Comservice.

|

The global telco NI market is spread across vendors of many stripes, some specializing in the telco market, some in IT services or software across verticals. Products range from fiber optic cables to core routers to OSS/BSS software to digital transformation services. And 5G is only one of many areas attracting telco investment right now. Plenty of vendors other than Huawei had good quarters in 2Q20, despite COVID-19 (and in some cases, because of it). There were also lots of laggards.

|

Based on YoY Telco NI revenue growth rates in 2Q20, winners include...CONTINUE READING

|

WNOs spend less on new facilities, more on servers, as annualized capex reaches all-time high of $114.4 billion; COVID-19 acting as accelerant

|

Economies across the globe remain ravaged by the COVID-19 pandemic, with high unemployment and steep declines in GDP. Yet webscale network operators (WNOs) reached all-time highs for a number of financial measures in 2Q20, including capital expenditures (capex), R&D expenses, and revenues. Free cash flow as a percent of revenues, or FCF margin, rose to 19.3% in 2Q20 on an annualized basis. That’s the highest since 4Q17. WNOs’ stockpile of cash and short-term investments reached $735 billion, up 11% YoY, and comfortably higher than WNO debt of $483 billion. Stock market valuations of key webscale players have climbed throughout the pandemic. The big are getting bigger, and fast.

|

Focusing on network investments, annualized capex grew 9% YoY to hit $114.4 billion in 2Q20; the network/IT portion of capex amounts to 49.7% of the total. Capex is highly concentrated in the webscale sector. The top 4 WNOs – Alphabet, Amazon, Google, and Facebook – accounted for 68% of the market for the four quarters ended 2Q20. That’s up from 63% of total capex in the 2Q19 annualized period. These 4 companies’ share of network/IT-focused capex is similarly high. That has implications for all sorts of markets, including semiconductors. It shouldn’t be surprising that chip sector consolidation has picked up as webscale providers have grown more dominant. Granted, semiconductor companies sell into a wide range of end use markets, notably consumer electronics and transport. But webscale players have become much more influential buyers as their data center footprints have expanded. That’s true even though WNOs do self-design some chips and partner with foundries for manufacturing.

|

|

As WNOs have grown, they’ve developed more sophisticated offerings in the cloud, often targeting specific vertical markets with customized platforms, including telecom...CONTINUE READING

|

|

|

|

To see our most recently published reports, click here

For information on subscribing to our research services, click here

|

|

You are receiving this because you are signed up to receive MTN Consulting's latest blogs and research alerts. We hope you enjoy our content, but you can unsubscribe at any time with the link at the bottom of this email - or by replying with "unsubscribe".

|

|

|

|

|

|

|