By Arun Menon

Summary

The battle is getting intense in the lucrative data center chips market amid supply chain shortages and delays caused by Covid-19 pandemic. Central to this battle is the Intel-AMD rivalry in which AMD seems to be attaining thrust, thanks to Intel’s production delays in the launch of its latest 10nm data center CPU, Ice Lake. Intel also delayed the launch of the next-generation Sapphire Rapids Xeon CPU to 1Q22. The costly delays have pushed Intel to boost its manufacturing and R&D capabilities: it will spend US$20B on two chip plants in Arizona and $600M for a chip R&D center in Israel. Despite the roadblocks, Intel still commands a dominant +90% share of the data center chips market. However, that share has been declining gently with AMD eating into the pie. One of the key reasons for AMD’s rise is its manufacturing strategy – it has transferred that burden to specialized foundries such as TSMC which boasts advanced process technologies. The result – AMD will be launching advanced 5nm EPYC Genoa chips next year, while Intel would still be offering 10nm (or Intel 7) Sapphire Rapids Xeon chips.

To spice up the competition further, GPU maker Nvidia will enter the server CPU market in 2023 with ARM-based CPU chips codenamed “Grace”. The move is a response to Intel’s bid to dent Nvidia’s stronghold in the server GPU market. Late last year, Intel launched its first GPU for data centers, Intel Server GPU. Also impacting sales prospects for Intel, AMD and Nvidia is the booming webscale sector of network operators: large WNOs are weaning off their Intel chip dependency by developing in-house chip designing capabilities. Further, a flurry of PE/VC-backed emerging start-ups developing data center chips is entering the scene. One of the key reasons for WNOs’ backward integration and start-ups disrupting the server CPU market is ARM. This pure play “design house” licenses its design architecture to both chip and tech companies for further customization and development, and it is gaining unprecedented traction in the data center space. And then there are geopolitical risks associated with semiconductors. As mentioned in our previously published report, clearly the semiconductor sector is an important element of the growing technology rivalry between the US and China.

With all these factors at play, Intel’s revamped leadership has announced several action items under its “IDM 2.0” strategy, including partnering with third-party foundries while keeping (and expanding) its fabs to overcome production roadblocks, along with extending its own foundry services by getting chip designers and webscalers to build customized chips on Intel’s fabs. While Intel’s plan to turnaround and reclaim leadership by 2025 looks strong, all eyes will be on the execution of plans from the new leadership – given the shift in market landscape and Intel’s own blemishes in the recent past.

- Table Of Contents

- Figure & Tables

- Coverage

- Visuals

Table Of Contents

- Abstract (p3)

- Executive Summary (p4-5)

- Data Center Architecture (p6-7)

- Data Center Server Layout (p8)

- Business Model (p9-10)

- Chipmaker Strategy & Roadmap for Data Centers: Intel, AMD, and Nvidia (p11-15)

- Product Offerings Analysis: Xeon vs. EPYC vs. Altra (ARM) (p16-17)

- Investments, Innovation, and Talent: Intel, AMD, and Nvidia (p18-19)

- Impact of WNO Backward Integration (p20)

- Chip start-ups to watch out for (p21-22)

- Appendix (p23)

Figure & Tables

- Data Center Architecture

- Data Center Server Layout

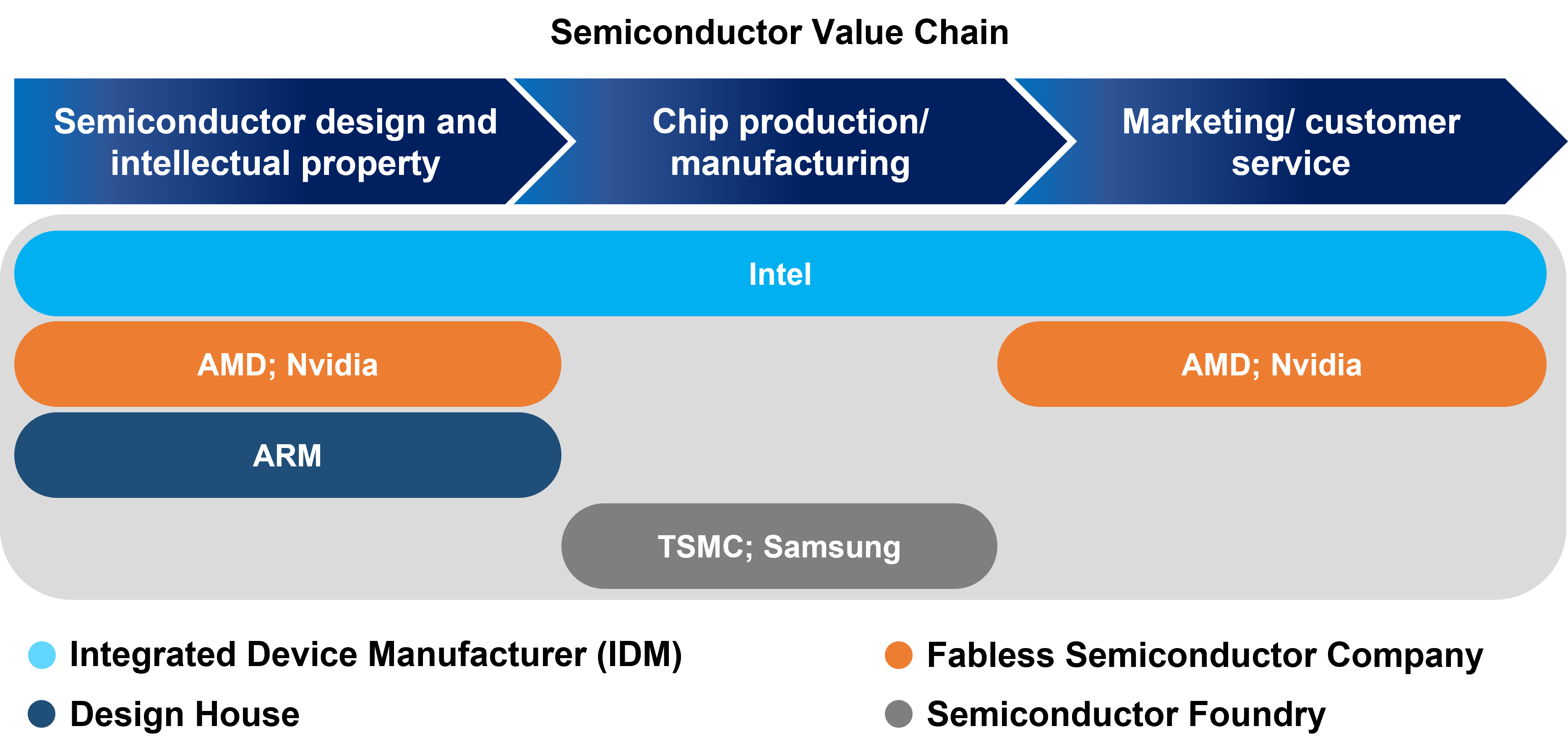

- Semiconductor Value Chain

- Data Center CPU Roadmap

- Data Center GPU Roadmap

- Top-of-the-Line Data Center CPU Comparison

Coverage

Companies and organizations mentioned in this report include:

Alibaba

Alphabet (Google Cloud Platform, or GCP)

Amazon (Amazon Web Services, or AWS)

AMD

Ampere Computing

Analog Devices

Annapurna Labs

Arm Holdings

Cerebras Systems

Cisco Systems

Enflame

Facebook

Fujitsu Limited

Fungible

GSK

Habana Labs

HPE

Intel

Juniper Networks

Lawrence Livermore National Laboratory

Los Alamos National Laboratory

Marvell Technology

Micron

Microsoft (Azure)

Nutanix

Nvidia

Qualcomm

Quanta Computer

RIKEN

Samsung Electronics

Shenzhen Baoan Bay Tencent Cloud Computing

SiFive

SK Hynix

Softbank Vision Fund

Swiss National Supercomputing Centre

Tachyum

Tencent

Tokyo Electron Devices

TSMC

Xilinx

Visuals