|

|

|

|

Website migration to mtn-c.com

|

Last week MTN Consulting migrated its website to a new domain. That brought with it some cosmetic tweaks, and improvements on the front end of our site to make navigation and search easier. On the back end, our content management system works much the same, so clients still have a similar look and feel to their dashboards.

|

With any site migration, lots of technical changes are required to make email, site analytics, google search, and other basic functions work effectively. If you work for a big company, you may take it for granted that the IT department has it covered, and never learn how complex and time-consuming all the adjustments can be. For a small company, the process is a bit more hands-on, to say the least.

|

Things are working fine now: emails are getting delivered and received, most importantly. However, if you are on this list and have a minute, please add matt@mtn-c.com to your contact list and/or flag the email as "not junk".

|

During the migration, we published two reports. It appears that a large number of users did not receive the alerts for these new reports. As such, this newsletter will provide a brief summary of both. One report is an interactive model which digs deep into telco opex, providing a standardized spend taxonomy and assessing which cost categories are growing/shrinking over time. The second is a short commentary on Nokia's recent analyst event.

|

A few stories we're tracking

|

Before summarizing the two MTN Consulting reports, here's a quick rundown of a small sample of the big recent industry news we are watching closely:

|

AWS announces Private 5G - the big cloud providers continue to edge into telecom markets. Already, AWS, Azure and GCP combine for over $2B in annualized revenues to the telecommunications vertical market. These top 3 cloud players are collaborating with many top telco-focused vendors for a variety of joint solutions. Now, AWS has announced an ambitious entry into the emerging market for private 5G solutions. The vendor landscape in telecom has shifted a lot in 2021 and change will accelerate in 2022.

|

FTC sues to block NVIDIA-Arm merger - MTN Consulting has always thought this deal would fizzle, and for good reasons: it would destroy lots of the value that Arm offers to the industry, and raises anti-competitive concerns. I always thought China would represent a big threat to the deal, but now it's clear that the US is even more of an obstacle. The UK is also taking a closer look.

|

VMWare spins off from Dell officially - VMWare has for several quarters been among the most successful vendors in growing share in the telco vertical. With its separation from Dell it will be interesting to watch what strategy shifts and/or investment expansions come as telcos rely even more on the cloud as 5G scales. As independent companies, both Dell and VMWare have made clear in recent weeks they have high hopes for the telecom vertical. VMWare, for instance, noted on its latest earnings call a major deal with Vodafone, which "selected VMware to deliver a single platform to automate and orchestrate all workloads running on its core networks across Europe, starting with 5G stand-alone...This recent work builds on Vodafone's previous selection of VMware Telco Cloud infrastructure as its network functions virtualization platform." Dell has recently introduced a "raft of servers for telco environments," and sees opportunities with open RAN projects, calling the RAN "the part of the network that has historically been dominated by proprietary equipment from vendors like Nokia, Ericsson, et cetera, that is opening up and creating opportunities for us."

|

DTAC and True may merge in Thailand - Thailand's 2nd and 3rd largest telcos aim to merge as they struggle to compete with market leader AIS. The merger would leave just two large telco groups in the country. AIS has succeeded by getting a head start on 5G and having a competitive fixed broadband offering on top of that, AIS Fiber. That's based in part on a 2017 acquisition we covered. A merger would raise serious anti-competitive concerns. It would also include an unusual shareholder mix: Telenor is the main overseas backer of DTAC, while China Mobile owns a stake in True.

|

|

American Tower buys CoreSite, converging its carrier-neutral infrastructure holdings - we have been expecting holders of carrier-neutral assets to diversify holdings across infra categories (data center, tower, and fiber), and that is happening more and more as time goes on. Private equity-led deals are responsible for much of this, but the latest is American Tower's $10B+ buyout of data center specialist CoreSite. This won't be the last deal in the space. One interesting angle is, to what extent might these larger CNNO entities begin to have excess market power in some of their territories? That could be good for their stockholders but it directly conflicts with the initial logic of having independent neutral providers. Recreating infrastructure monopolies is not what the industry should be aiming for.

|

|

|

|

MTN Consulting’s Telco Opex Analyzer analyzes the opex trends of a subset of key telcos in the telecommunications sector. The report’s dashboard allows a user to dig into overall spending levels, network’s contribution to opex, network-related capex, and profitability for a group of 21 individual operators. The report is designed to help vendors understand and plan for the needs of their customers and help network operators deploy their technology budgets wisely. The report’s format is Excel.

|

Telcos have faced flat revenues for many years. After adjusting for exchange rate fluctuations and COVID-19, top-line growth has been in the 1-3% per year range, for many years. That compares to double digit growth rates in the webscale sector. As a consequence, telcos have been focused on their cost base in search of profitability growth. Costs include both capital expenditures (capex) and operating expenses (opex). Many MTN Consulting reports analyze capex. That’s in line with the traditional focus of most vendors, who historically sell more into capex budgets than opex. Opex is rising in importance to vendors, though, and as a cost category it is several times the size of capex. Further, for telcos seeking success, understanding and effectively managing opex is crucial. Telco earnings reports make this obvious, as they highlight things like opex transformation programs, careful opex management, cost optimization initiatives, network efficiencies, and process automation.

|

The problem is that opex is a bit of a mystery – it’s hard to understand across companies, countries, and over time. Reporting categories, definitions, and accounting standards vary widely. This report solves the problem. We have created a taxonomy of opex categories, examined a broad cross-section of telcos, and calculated a detailed opex profile for both the individual companies and the overall telecommunications industry (see Figure 1, below). Key findings include:

|

|

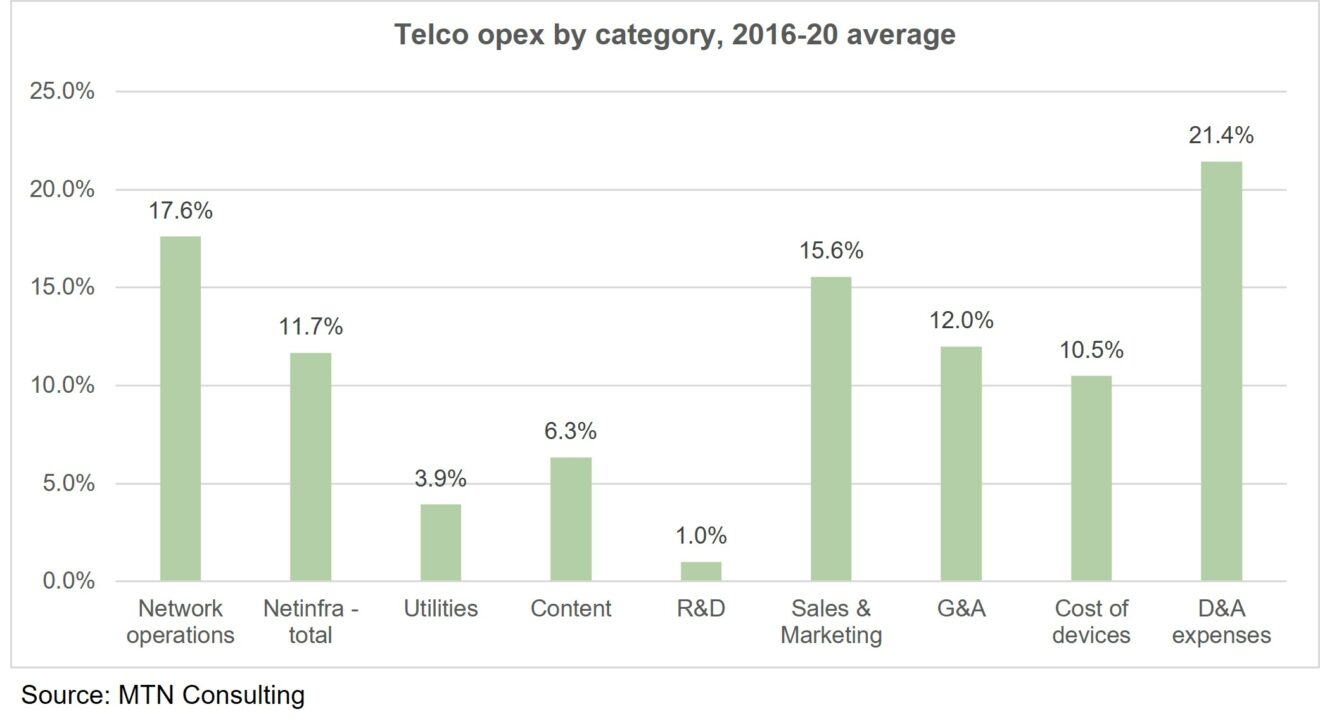

(1) The sum total of all network-related opex – including network operations, netinfra (leasing, interconnection, and spectrum fees), utilities (90%), and depreciation (85%) – amounts to a whopping 51% of total opex, on average. The network-related opex share can get as high as 70% (Veon) or 80% (Airtel) for some companies. For telcos, the network is their factory.

|

|

|

Figure 1: Telco opex by category, 2016-20 average

|

|

|

|

|

(2) Network operations opex alone accounted for an average 17.6% of total opex for telcos in the 2016-20 timeframe, and there is upwards pressure on this figure. Further, network operations opex can vary dramatically across companies, exceeding 20% of total opex for many companies, and over 30% for at least one telco in our study (Telkom Indonesia)

|

(3) Netinfra opex fell dramatically in 2019 due to implementation of a new accounting standard (IFRS 16), but increased depreciation and amortization expenses offset this decline.

|

|

(4) Utilities, content, and R&D opex average to 4%, 6%, and 1% of total opex, with lots of variation around these averages: Airtel spends about 11% of opex on utilities, content accounts for over 35% of total opex for Comcast, and BT is a big spender on innovation with R&D accounting for over 3.5% of total opex...[READ MORE]

|

|

|

|

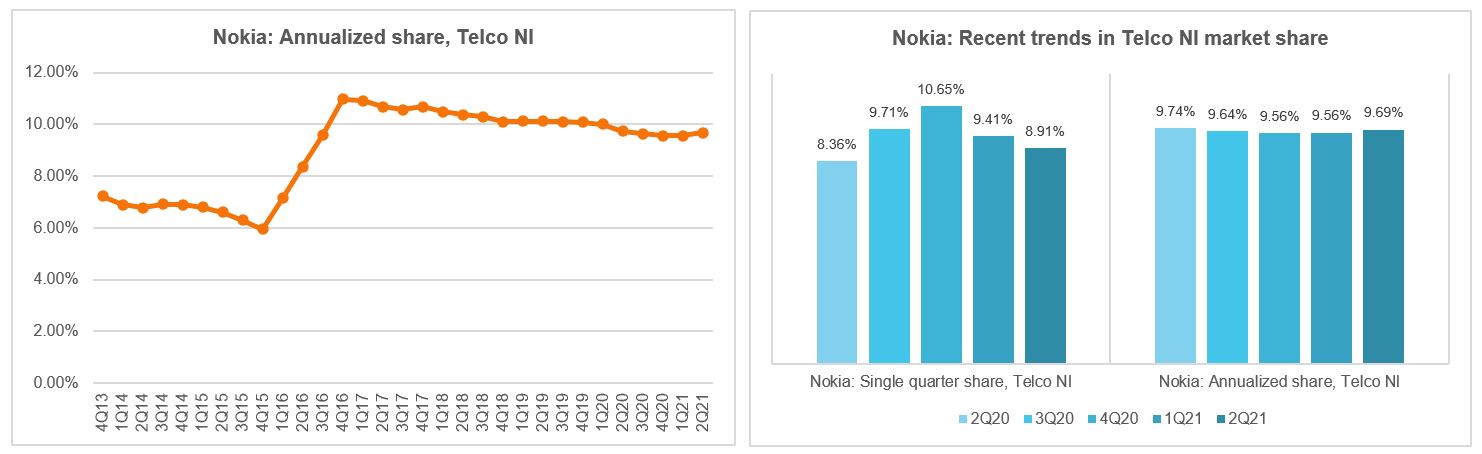

Nokia held an online forum for industry analysts last week. Over four days of presentations, the company presented a compelling case for why it will remain a top tier supplier to telcos as they evolve networks and business models over the next 5-10 years. The company also highlighted strong positioning for new opportunities related to webscale/cloud and private (enterprise) networks. In the telco network infrastructure (telco NI) market, Nokia is #3 behind Huawei and Ericsson, but #2 (behind only Huawei) if you exclude services. It has a comprehensive offering across mobile, fixed broadband, optical, IP, subsea, and software, and has strong R&D chops. In the webscale/cloud world, Nokia is a relative newcomer but was among the earliest big telco-focused vendors to launch deep collaborations with the three main cloud players.

|

|

|

Figure 2: Nokia's share of telco network infrastructure market

|

|

|

|

|

Further, it has reorganized the company to go after “cloud and network services” opportunities. The company is credible when it talks about the importance of sustainability, which deserves far more attention than it gets, and which Nokia’s customers will care more about every year as energy bills rise and climate change worsens. While Nokia has plenty of competition in both its core telco and cloud/enterprise markets, the weakening of Huawei in the last 3 years is another boost for the company. The future looks good for Nokia. [MORE INFO]

|

|

|

|

|

VIEW MORE MTN CONSULTING NEWSLETTERS HERE

|

|

|

|

To see our most recently published reports, click here

For information on subscribing to our research services, click here

|

|

You are receiving this because you are signed up to receive MTN Consulting's latest blogs and research alerts. We hope you enjoy our content, but you can unsubscribe at any time with the link at the bottom of this email - or by replying with "unsubscribe".

|

|

|

|

|

|

|