|

|

|

|

This is MTN Consulting's fourth regular newsletter to subscribers. This edition comments on recent vendor earnings & telco capex results, and China's 5G rollout.

|

|

|

_____________________________________________________________________

|

|

Telco NI vendor revenues up 0.4% YoY

|

Network spending in the telecom network operator (TNO/telco) sector remains constricted. Telcos are virtualizing their networks, transforming their operations, renting more of their network resources, and taking a modest approach to network upgrades. Competition is tight on the vendor side, even without Huawei involved in everything. The result in 3Q19 is a flat market, overall.

|

Over 90% of market has reported

|

For 81 vendors, including acquired divisions, we have now estimated total revenues and revenues to the telco vertical in 3Q19. That amounts to well over 90% of the market.

|

Huawei is always a complicating factor, so first consider growth without Huawei. For all vendors excluding Huawei, revenues to telcos ("Telco NI") grew 0.6% YoY in 3Q19, about the same rate as the +0.7% growth rate for the same group in 2Q19. For just Huawei, reliable data is limited, but our working estimate is that Huawei's sales fell -0.2% in 3Q19. That's an improvement from -6.1% in 2Q19. For all vendors, including Huawei, market growth in vendor sales to telcos was about 0.4% in 3Q19. Assuming the Huawei growth rate is correct, this represents a modest upswing from 2Q19 when vendor revenues dropped -1.1%.

|

Our "Telco NI" tracking considers vendor revenues in services and software, not just hardware. As such Telco NI vendors are dependent on a mix of their customers' opex and capex budgets. However, capex is the primary driver, and has a close correlation with vendor revenues.

|

In 2Q19, total telco capex grew 5% YoY on the back of a China surge. However, in 3Q19, for a sample of 36 reporting telcos (all outside China), capex grew at a +0.2% YoY rate. That's down from +3.4% in 2Q19 for the same sample of 36. Revenues for the group of 36 grew 1.7% in 3Q19, quite a bit faster than the group's capex.

|

The telco results for 3Q19 are very preliminary - we track 130 telcos in total - but vendors won't take much comfort from the results to date. Guidance also tends to be moderate. These numbers don't include any Chinese operators, and China's telco capex may well surge again in 3Q19. However, non-Chinese vendors are having an even tougher time than usual in China. Cisco is an example. Its reported sales in China dropped 31% YoY in 3Q19. Life has always been hard in China for overseas vendors, but it's gotten worse. Foreign vendors angling for a share of the local 5G market face an uphill battle.

|

Given the tight spending climate mixed with the rise of software and the race to 5G, M&A activity in the vendor sector should remain vigorous. Just today Ribbon announced it would acquire ECI, for instance. That adds to a number of significant deals recently announced or completed in the sector, including: Ciena-Centina, Ericsson-Kathrein, Casa Systems-Netcomm, Cisco-Acacia, Intel-Barefoot, CapGemini-Altran, and others. More will follow, as 5G spreads.

|

|

--Matt Walker, Chief Analyst

|

|

|

_____________________________________________________________________

|

China rolls out 5G despite earnings challenges and low demand for 5G smartphones

|

|

China’s big three telecom operators—China Mobile, China Telecom and China Unicom—officially launched 5G service in 50 cities nationwide on November 1st. In advance of the launch, the big three telcos recorded 10 million pre-orders of the 5G service, according to the State Council of the People’s Republic of China. Of this total, China Mobile accounts for 5.9M while China Telecom and China Unicom add 2.1 and 2.0M respectively.

|

With this 50-city launch, China’s telcos are setting themselves apart from their US counterparts, who are rolling out the service only in select cities at a time. 5G was launched nationwide in South Korea and in a few cities in the US and the UK, China’s sheer scale makes it stand out. The Chinese government, for instance, claims local operators will roll out in excess of 130K base stations (from the current levels of 86K) by the end of 2019. For comparison sake, consider UAE-based Etisalat, which gets a lot of attention as a 5G early mover. Etisalat is deploying 900 5G base stations over the 2019-20 period to support its early 5G rollout.

|

Wide scale adoption of 5G is not without challenges

|

The official launch of a 5G service is only step 1, as there are many roadblocks to adoption.

|

One major obstacle for wide scale adoption of 5G is its price point. Though 5G prices appear to be cheaper than 4G when compared on a per gigabyte basis, a basic 5G plan is pricier than 4G. While 4G service starts at around RMB38 ($5) per month, a basic 5G monthly plan costs RMB128 ($18). That includes data consumption of 30GB, but with a maximum speed of just 300Mbps. This speed is high in comparison to average 4G speeds of 25Mbps, but far behind telco claims of 1Gbps speed. Further, the service can be used only after buying a 5G-compatible phone, making it more costly.

|

High priced handsets could also hinder the growth of 5G. For instance, an entry level 5G phone (Vivo’s iQOO Pro) is priced at RMB3,798 ($540), and the top end Huawei 5G phone (Mate X) is priced at RMB16,999 ($2,400). The Mate is much costlier than Apple’s high end iPhone 11 Pro Max, which is little over $1,500. Handset prices will not reach similar levels to 4G anytime soon. The 5G handsets are priced heavily mainly due to usage of costly components, IP rights and R&D. Specific use cases will be needed to stimulate demand, and handset subsidies will often be required.

|

|

Margin pressure and 5G’s demands entice network sharing

|

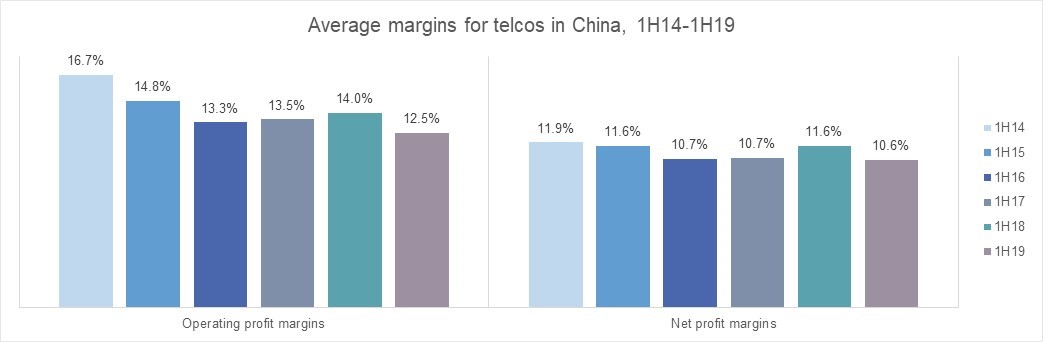

As the big three telcos launch their 5G services, average profit margins in the industry have been on the decline. For the first six months of 2019, operating and net profit margins for the three telcos combined reached 12.5% and 10.6%, respectively, from 14.0% and 11.6% in 1H18 (figure, below). These were the weakest results recorded since 1H14.

|

|

|

|

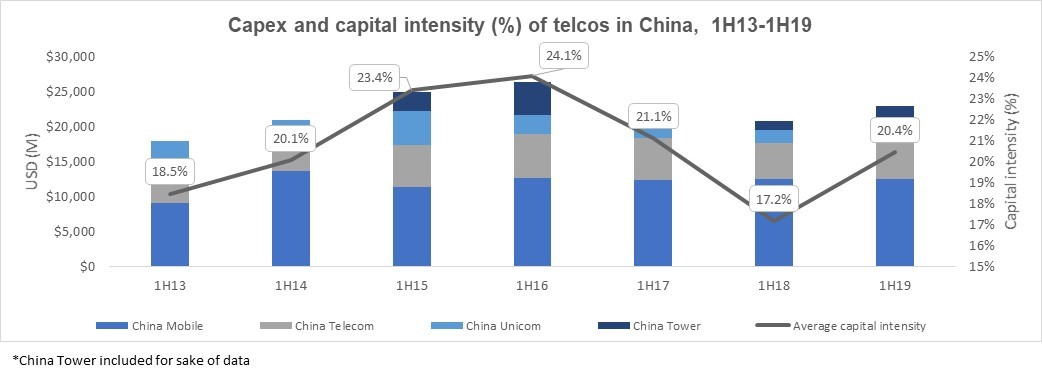

As margins moderate, Chinese telcos also face high 5G network construction costs. Already their capital spending has spiked, as shown in the figure below.

|

|

|

|

Capital intensity for the industry remains below the peaks seen in 1H15 and 1H16, but the market has become more competitive now and operators more cost conscious. Pushing capex above 20% of revenues is not an easy thing to justify.

|

To cut costs as well as risks, telcos are turning to network sharing. In August China Telecom and China Unicom signed an agreement to share a 5G RAN in 15 major cities. China Unicom's Chairman Wang Xiaochu said “5G network-sharing could save it between 200 billion yuan to 270 billion yuan ($28.2 billion to $38.1 billion)”. These numbers are somewhat speculative and implementation will have challenges. However, there are clear cost benefits from network sharing in 5G as the sector moves towards integrating new and existing spectrum frequency bands for 5G and densifying networks.

|

Despite 5G’s costs, operators hope that the 5G rollout will present new avenues for revenue growth, justifying the early push. There is also a political element to 5G. The government is hoping an early launch of 5G will give China the power to set global standards for networks in the future, and drive its technology leadership in areas such as connected cars, virtual reality and IoT. Chinese technology suppliers such as Huawei benefit from big, early rollouts within China, in terms of getting costs down, and getting credibility up as they market their wares overseas. We expect China's government to continue hyping up its early 5G efforts, and helping position local companies for overseas growth in related fields.

|

--Subramanian Venkatraman, Principal Analyst

|

|

|

____________________________________________________________________

|

"Telecom's biggest vendors: 2Q19" - Summary version available

|

|

To get up to speed on the market for network infrastructure sales to telecom operators ("Telco NI"), we are offering newsletter subscribers a complimentary report. This short report is based upon our full interactive Excel model, Telecom's biggest vendors: 2Q19. To download the free version, click below:

|

|

|

|

|

|

|

|

To see our most recently published reports, click here

For information on subscribing to our research services, click here

|

|

You are receiving this because you are signed up to receive MTN Consulting's latest blogs and research alerts. We hope you enjoy our content, but you can unsubscribe at any time with the link at the bottom of this email - or by replying with "unsubscribe".

|

|

|

|

|

|

|

|

|